Self Custody Wallet Rules: Custodial vs Non-Custodial Crypto

Self custody wallet rules: custodial vs non-custodial crypto

What is a self custody wallet?

A self custody wallet is a crypto wallet where you, not an exchange or wallet company, control the private keys that approve movement of your digital assets. If you keep the recovery phrase safe, you can move funds without asking a custodian for permission.

Why it matters: Custody affects control, recovery, privacy, tax records, sanctions exposure, insurance, and what happens if a platform fails. A custodial account can feel easier because the provider handles login recovery and some reporting. A self-custody setup removes custodian failure risk, but it also makes you responsible for security and documentation.

The common story is that self-custody is always safer and more private. That is only partly true. Self-custody protects you from a platform blocking withdrawals or becoming insolvent. It does not make blockchain activity invisible, erase tax duties, or protect you from bad signatures. In 2026, the better question is not “which wallet is purest?” It is “which custody model gives me the right balance of control, recovery, and compliance for this specific use?”

For a dated reference point, FTX disclosed that its 50 largest unsecured creditors were owed about $3.1 billion after its bankruptcy filing (Reuters, November 2022). That event made counterparty risk easy to understand. It did not remove the separate risks that come with holding keys yourself.

Key terms: wallet, private key, seed phrase, address

A crypto wallet is software or hardware that manages blockchain addresses and signs transactions. It does not store coins inside the device. The assets are recorded on the blockchain, while the wallet stores or controls the credentials needed to move them.

- Private key: A secret cryptographic credential that authorizes outgoing transactions. Anyone with the private key can move the funds.

- Seed phrase: A recovery phrase, usually 12 or 24 words, that can restore access to the wallet. If someone else gets it, they can take the assets.

- Public address: The string of letters and numbers you share to receive funds. It is visible on-chain, but it does not let another person spend from the wallet.

- Wallet software or hardware: The app, browser extension, smart contract wallet, or hardware device that helps you approve transactions.

Andreas Antonopoulos, author and educator, is widely associated with the custody principle often summarized as “not your keys, not your coins.” The phrase is simple, but the regulatory lesson is more detailed: key control changes who can act on the funds and who must keep records.

Why regulation cares about custody

Regulators usually start with a practical question: who is the intermediary? If a company holds customer assets, transfers funds, or converts crypto to fiat money, that company may have identity-check, monitoring, and reporting duties. If you hold your own keys and transact directly, there may be no custodian in the middle, but your personal tax and sanctions duties still remain.

By May 2026, the clearest user rule is this: control and responsibility move together. A self-custody wallet can reduce platform risk, yet it can increase recordkeeping pressure. You need a system for cost basis, transaction dates, counterparties, wallet addresses, and the purpose of transfers.

Custodial vs non custodial wallets: the core difference

The core difference in custodial vs non custodial wallets is private key control. In a custodial wallet, the provider holds the keys and moves crypto for you. In a self-custody wallet, you hold the keys and approve transactions yourself.

How a custodial wallet works

A custodial wallet is usually an exchange account or brokerage app. You log in with an email, password, and often two-factor authentication. The provider keeps the private keys and updates your account balance internally. This is convenient because customer support may help with account recovery, tax exports, and security alerts.

The tradeoff is control. A custodial provider can freeze withdrawals, comply with court orders, pause activity during an incident, or fail as a business. The user owns a claim against the platform, not direct control of the private keys. For new users or active traders, that tradeoff can still be reasonable if the provider is regulated and security habits are sound.

How a self-custody wallet works

With a self-custody wallet, your phone, browser wallet, hardware wallet, or smart contract wallet signs transactions using keys you control. No exchange signs on your behalf. That direct control is why many users compare a hardware wallet vs exchange setup before moving long-term holdings away from a platform.

The downside is finality. If you lose the seed phrase, send funds to the wrong address, or approve a malicious contract, there may be no support desk able to reverse the mistake. Self-custody is powerful because it removes an intermediary. It is demanding for the same reason.

Feature | Custodial wallet | Self-custody wallet |

|---|---|---|

Control | Provider controls private keys | User controls private keys |

Recovery | Password reset and support may be available | Seed phrase or recovery setup is the main backup |

KYC | Usually required before trading or withdrawals | Usually not required by the wallet itself |

Transaction freezes | Provider or legal order may block activity | Third parties cannot freeze the wallet directly |

Privacy | Identity is linked to the account | Address is pseudonymous, but on-chain activity is public |

Responsibility | Shared with the provider | Falls mainly on the user |

Background: how crypto custody regulation evolved by 2026

Crypto custody rules grew from two pressures: consumer losses at centralized firms and the use of crypto rails in cross-border payments. Regulators did not ban self-custody in major markets. Instead, they focused on intermediaries that hold funds, exchange assets, or connect crypto to the banking system.

From key-control culture to reporting rules

In the early years of Bitcoin, self-custody was mostly a technical and philosophical practice. Users who controlled their keys did not depend on a bank or exchange. After 2022, that idea became practical risk management. Platform failures showed that exchange balances are exposed to business, legal, and operational risk.

At the same time, governments expanded reporting rules for businesses that handle crypto. The EU’s MiCA crypto rule became applicable for crypto-asset service providers from 30 December 2024 (ESMA, December 2024). In the U.S., final broker reporting rules require certain brokers to report digital asset sales and exchanges, with gross proceeds reporting beginning for transactions in 2025 (IRS, June 2024).

Regulatory labels readers should know

Term | Plain-English meaning |

|---|---|

KYC | “Know your customer” checks, where a service collects identity information before allowing certain activity. |

AML | Anti-money-laundering rules that require financial businesses to monitor and report suspicious activity. |

Travel rule | A rule requiring covered crypto businesses to share sender and recipient information for qualifying transfers. The FATF standard uses a USD/EUR 1,000 threshold (FATF, June 2019). |

VASP | A virtual asset service provider, such as an exchange or custodian that handles crypto for customers. |

Hosted wallet | A wallet where a provider holds the private keys for the user. |

Unhosted wallet | A self custody wallet where the user controls the keys without a custodian. |

Qualified custodian | A regulated institution that holds assets for clients under legal and operational requirements. |

Hester Peirce, commissioner at the U.S. Securities and Exchange Commission, has repeatedly argued in public remarks that crypto rules should be clear enough for builders and users to understand before enforcement becomes the main guide. For everyday wallet users, that means paying attention to the line between software that lets you hold keys and services that handle funds for you.

Regulatory implications of using a self custody wallet

Using a self custody wallet is legal in most major jurisdictions, including the U.S., UK, EU, Canada, and Australia. The regulatory issue is not possession of a wallet. It is the activity connected to that wallet.

To make the decision less abstract, we use the custody liability map, an original 2026 decision framework for everyday users. It asks three questions before each action: Who controls the keys? Who sees the identity data? Who must keep the tax and compliance record?

Our 2026 custody decision map

The table below is an editorial dataset built in May 2026 from common user actions, public reporting rules, and wallet behavior. It is not legal advice. It is a practical way to compare risk signals before choosing custody.

User action | Custody type involved | Regulatory signal | User record to keep |

|---|---|---|---|

Buy crypto on a regulated exchange | Custodial | KYC and broker reporting may apply | Trade date, amount, fees, cost basis |

Withdraw to a hardware wallet | Custodial to self-custody | Exchange logs the destination address | Withdrawal address, transaction ID, cost basis |

Hold assets for one year | Self-custody | No sale by itself, but records still matter | Wallet inventory and backup location note |

Swap tokens through a protocol | Self-custody plus smart contract | Possible taxable disposal and approval risk | Fair market value, fees, contract address |

Bridge assets across chains | Self-custody plus service | Counterparty and sanctions screening matter | Bridge used, source chain, destination chain |

Send funds to another person | Self-custody | Purpose and counterparty risk matter | Recipient address, reason, date, value |

Sell back through an exchange | Self-custody to custodial | Exchange and tax agency may receive data | Deposit address, sale proceeds, gain or loss |

Use hosted recovery or in-app fiat services | Hybrid | A third party may have compliance duties | Terms accepted and provider name |

Tax reporting does not disappear

Moving crypto from an exchange to your own wallet is usually not a taxable sale by itself. Selling, swapping, spending, earning, or receiving crypto as income may create a taxable event. The wallet type does not decide the tax result. The activity does.

Example: a user buys 0.5 BTC on an exchange in March 2025, withdraws it to a hardware wallet, and sells it in January 2026 through a different service. The withdrawal is mainly a recordkeeping event. The later sale may create a capital gain or loss. If the user has messy transaction history, knowing when to hire a crypto tax accountant can prevent avoidable filing errors.

In the U.S., the IRS has said broker reporting rules for digital asset gross proceeds begin with transactions in 2025 (IRS, June 2024). Self-custody users may still receive fewer third-party forms for peer-to-peer activity, which makes personal records more important, not less.

AML and sanctions risk

AML rules apply mainly to financial businesses, but sanctions restrictions can affect individuals too. The U.S. Treasury sanctioned Tornado Cash-related smart contract addresses on 8 August 2022 (U.S. Treasury, August 2022). That action showed that wallet addresses and smart contracts can become part of sanctions compliance, even when users are operating outside a custodial exchange.

The practical risk for most ordinary users is not that every small transfer will be investigated. The risk is that a large transfer, bridge, mixer, or counterparty later appears connected to stolen funds or a sanctioned actor. Before sending significant value, check the service, check the address history when possible, and avoid tools designed to hide origin of funds.

When wallet providers may face rules

A wallet app that only lets you hold keys and sign transactions locally is different from a service that holds funds, swaps tokens for you, provides fiat on-ramps, or offers hosted recovery. The more a wallet app acts like a financial intermediary, the more likely the provider has its own compliance duties.

This matters because many products mix features. A browser wallet may be non-custodial for storage but rely on third parties for swaps, card purchases, staking, or recovery. Understanding how securities law applies to crypto is useful when a wallet connects to tokens, staking programs, or DeFi protocols.

Brian Armstrong, co-founder and chief executive of Coinbase, has often framed custody and usability as linked adoption questions. That is a helpful reminder for users: the easiest product may involve more intermediaries, while the most direct custody model may demand more personal skill.

The three-layer responsibility test

Use this original test before moving meaningful funds into self-custody:

- Tax layer: Can you prove cost basis, date, amount, and fair market value for each taxable action?

- Counterparty layer: Do you know whether the address, protocol, bridge, or service is connected to obvious illicit or sanctioned activity?

- Custody layer: Do you understand whether any feature of the wallet lets a third party hold, recover, or move funds?

If you cannot answer yes to all three, the problem is not self-custody itself. The problem is that the chosen workflow needs more preparation.

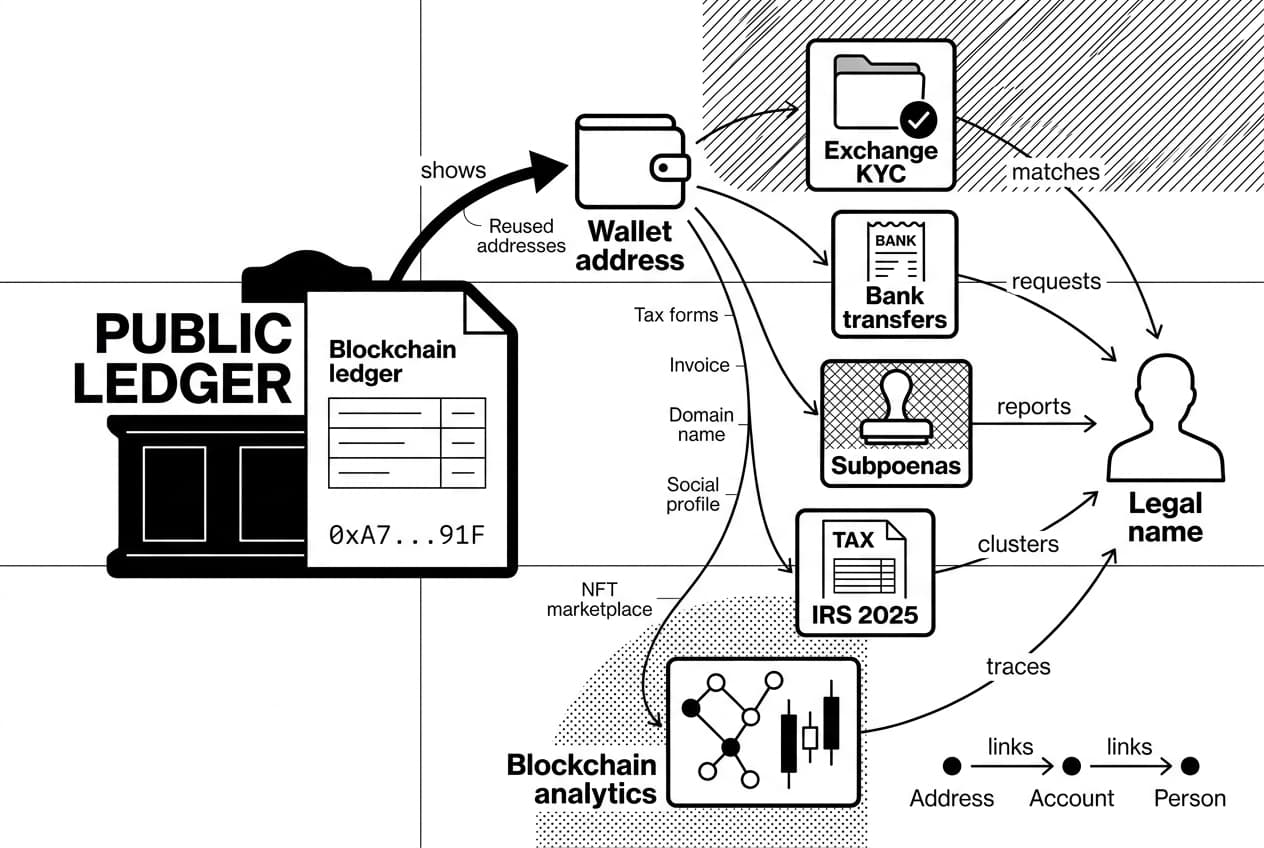

Can regulators see a self-custody wallet?

A self-custody wallet is pseudonymous, not anonymous. Your address does not show your legal name on-chain, but the transactions are public. Regulators may connect the address to you through exchange withdrawal records, bank activity, subpoenas, reused addresses, tax forms, or blockchain analytics.

A public blockchain resembles a courthouse records desk: anyone can inspect the ledger, and old entries stay visible. The hard part is not seeing the transaction. The hard part is linking the address to a person. Once an address touches an exchange account with identity checks, that link may already exist in private records.

Pseudonymous does not mean anonymous

A wallet address is just a string of letters and numbers. It becomes easier to identify when it connects to a regulated exchange, invoice, domain name, social profile, NFT marketplace account, or repeated transaction pattern. A single public post can connect a wallet to a person. So can a deposit from a known exchange account.

For more background on identity leakage, read our guide to blockchain pseudonymity. The short version is that privacy requires planning. It is not the default setting on public chains.

How tax agencies may connect the dots

Tax agencies do not need to break encryption. They can compare exchange records, bank transfers, reported sales, blockchain data, and documents obtained through legal process. The IRS has public guidance explaining virtual currency reporting duties (IRS, updated 2025), and broker reporting rules add another data source for covered transactions.

Analytics firms can cluster addresses, trace flows, and flag interactions with known services. To learn how that works, see how blockchain surveillance works. The point is not panic. The point is to keep records that match what the chain and your exchange history already show.

- Pseudonymity is limited: an address can become identifiable after it touches a known account or public profile.

- Public chains preserve history: old activity can be reviewed years later.

- Tax agencies use many sources: exchange data, tax forms, bank records, analytics tools, and subpoenas can all matter.

- Good records help: wallet addresses, dates, transaction IDs, and cost basis make reporting easier.

Risks, protections, and compliance steps for self-custody

Using a self custody wallet gives you direct control, but it also removes many safety nets. Before focusing on advanced privacy or DeFi strategies, get the basic security and compliance routine right.

Security risks: lost keys, phishing, malware, and bad approvals

The seed phrase is the master recovery tool. If it is lost, destroyed, photographed by malware, typed into a fake site, or stored in a hacked cloud account, the wallet can be emptied or permanently inaccessible. There is no standard password reset for a normal self-custody wallet.

Phishing is common because attackers do not need to hack the blockchain. They only need to trick the user into signing the wrong message or revealing a recovery phrase. Malware can also replace copied addresses before you paste them. DeFi users face approval risk too: a token approval can give a smart contract permission to spend assets later. If you have used DeFi, learn how to revoke token approvals and make review part of your routine.

A hardware wallet can reduce many online attack paths by keeping private keys offline. If you are moving meaningful funds for the first time, read how to set up a Ledger wallet before sending more than a small test amount.

Compliance checklist before you withdraw

- Verify the destination address on the hardware wallet or trusted wallet screen before sending funds.

- Record your cost basis for each asset before it leaves the exchange.

- Save the transaction ID, date, amount, sending address, and receiving address in a tax tool or spreadsheet.

- Avoid sanctioned services by checking official lists and avoiding mixers or bridges with known illicit links.

- Test with a small transfer before moving the main balance.

- Secure your seed phrase offline, preferably with a backup stored separately from the device.

- Review active approvals after using DeFi apps, then revoke permissions you no longer need.

- Document future disposals with fair market value, fees, and purpose at the time of each sale, swap, or spend.

- Review your setup yearly, especially after moving countries, changing exchanges, or increasing holdings.

Insurance and recovery tradeoffs

Custodial platforms may carry crime coverage, use segregated accounts, or offer institutional custody arrangements. Those protections can help, but they are narrower than many users assume. Policies may exclude user error, social engineering, insider conduct, or losses outside the provider’s control. Our guide to crypto insurance explains these limits in more detail.

With self-custody, insurance and recovery are usually personal design problems. You decide how backups are stored, who knows they exist, how heirs can recover assets, and how much value sits in one wallet. The best setup is not the most complex one. It is the one you can follow consistently without exposing the seed phrase.

How to choose between self-custody and a custodial wallet

Neither model is always better. The right choice depends on the amount involved, your security skill, your need for recovery support, your tax complexity, and whether you need to use DeFi tools.

A beginner buying a small amount of crypto may be safer starting with a regulated custodial platform while learning. A long-term holder with a larger balance may reasonably move most assets to a hardware wallet after practicing backups and test transfers. A business, trust, or fund may need a qualified custodian for governance and audit reasons.

Best fit by user type

User profile | Often better fit | Reason |

|---|---|---|

New buyer | Custodial | Account recovery and simple tax exports reduce early mistakes. |

Long-term holder | Self-custody | Cold storage reduces exchange insolvency and withdrawal-freeze risk. |

DeFi user | Self-custody | Most DeFi protocols require direct wallet signatures. |

Active trader | Custodial | Liquidity, order books, and fast execution are easier on exchanges. |

Business treasury | Qualified custodian or governed multisig | Controls, audit trails, and fiduciary duties matter more than convenience. |

Privacy-conscious user | Self-custody with careful records | KYC data stays off the wallet layer, but chain activity remains visible. |

A practical hybrid custody model

Many users do not need to choose one model for everything. A practical split is to keep a smaller operating balance on a regulated exchange for purchases or trading, and move long-term holdings to a hardware wallet. For example, a user might keep $500 to $1,000 on an exchange for near-term activity and store long-term BTC or ETH offline (Investor.gov, May 2024 provides general crypto asset risk education).

We call this the split-by-purpose rule: exchange for activity, self-custody for savings. The exact percentage can change as your skills and holdings grow. What should not change is documentation. Every movement between custody types should include the date, amount, transaction ID, wallet address, and cost basis.

- Match custody to purpose: trading, long-term saving, DeFi, and business treasury needs differ.

- Do not overestimate privacy: self-custody removes a custodian, not public chain history.

- Start small: practice test transfers before moving large balances.

- Review as holdings grow: a setup that works for a small balance may not fit a larger portfolio.

Frequently Asked Questions

- Can the IRS know about a self-custody crypto wallet?

- A self-custody wallet has no name attached on-chain, but the IRS can connect it to you through exchange withdrawal records, bank transfers, blockchain analytics firms, subpoenas, or reused addresses. Reporting all taxable transactions accurately and maintaining thorough records remains a legal obligation regardless of wallet type.

- What is the best self-custodial crypto wallet?

- There is no single best option for everyone. The right wallet depends on which assets you hold, whether you need DeFi access or long-term cold storage, open-source transparency, hardware compatibility, recovery design, and your comfort with technical responsibility. Evaluate each wallet against your specific security and usability needs.

- Is Coinbase Wallet a self-custody wallet?

- Yes, Coinbase Wallet is generally self-custodial because you control the recovery phrase and private keys. This is different from a standard Coinbase exchange account, where Coinbase holds the keys on your behalf. The branding is easy to confuse, so always confirm who actually controls the private keys before storing funds.

- What is the difference between a self-custody wallet and an exchange?

- A self-custody wallet lets you control private keys and sign transactions directly. An exchange holds assets on your behalf and maintains internal account balances. Exchanges typically require KYC, can freeze accounts, and offer customer support for recovery. Self-custody wallets offer greater control but no safety net if keys are lost.

- What is the difference between custodial and non-custodial wallets?

- Custodial wallets place a third party in control of your private keys, offering convenience and account recovery at the cost of control. Non-custodial wallets put key management entirely in your hands, giving you full ownership of assets but full responsibility for security. Neither type is universally superior — the tradeoff depends on your priorities.

Sources

Author

Crypto analyst and blockchain educator with over 8 years of experience in the digital asset space. Former fintech consultant at a major Wall Street firm turned full-time crypto journalist. Specializes in DeFi, tokenomics, and blockchain technology. His writing breaks down complex cryptocurrency concepts into actionable insights for both beginners and seasoned investors.