Crypto Insurance: Is Your Digital Asset Portfolio Safe?

Crypto Insurance: Is Your Digital Asset Portfolio Safe?

What Is Crypto Insurance?

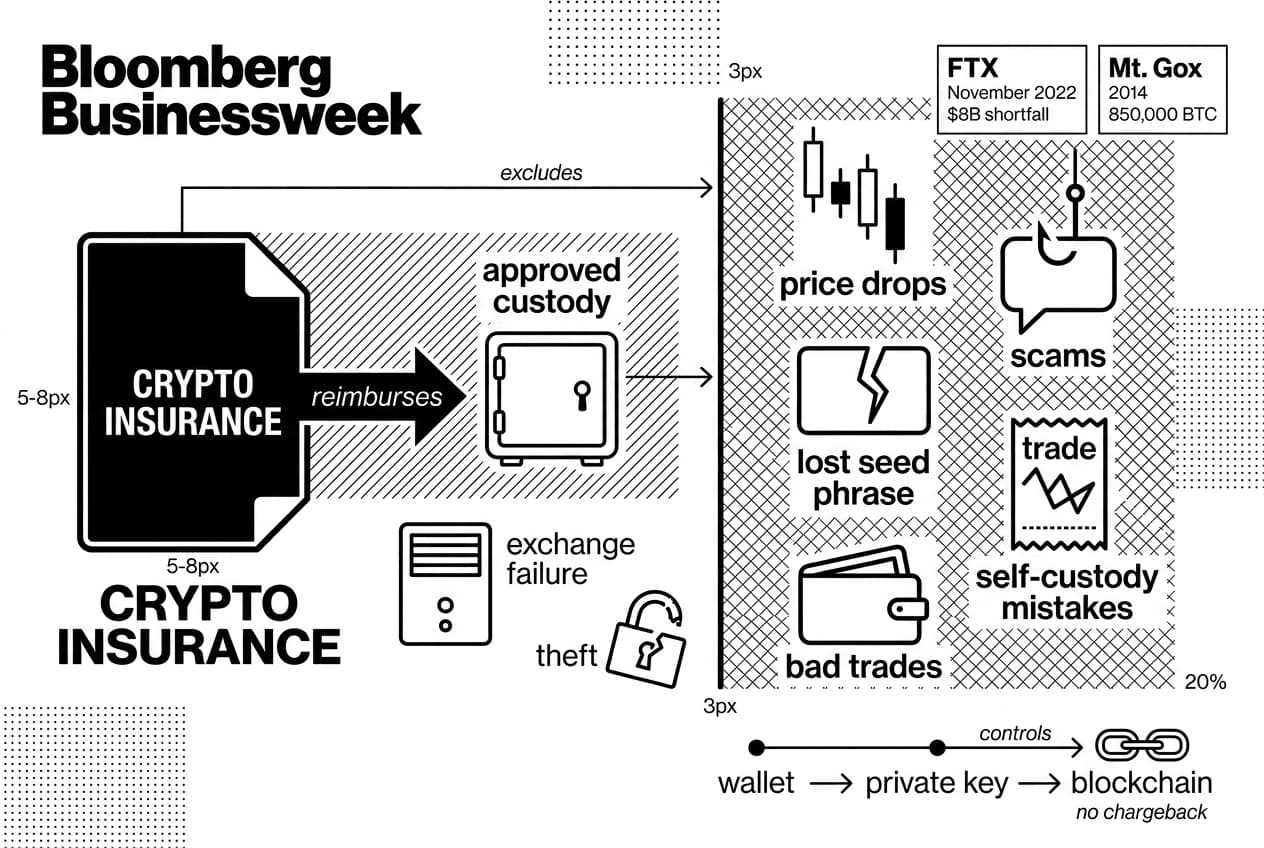

Crypto insurance is coverage designed to reimburse specified digital-asset losses, such as theft from approved custody systems or certain exchange security failures. It does not cover every crypto risk. Price drops, scams, lost seed phrases, bad trades and many self-custody mistakes are usually excluded.

Why It Matters

Digital assets are cryptocurrencies or tokens controlled by cryptographic keys on a blockchain, which is a shared public ledger. A wallet is the software or hardware that lets you use those keys. A private key is the secret credential that proves control. If a key is stolen or lost, the asset can disappear from your reach without a bank branch, card network or chargeback desk to reverse the mistake.

The stakes are not theoretical. FTX collapsed in November 2022 with an estimated $8 billion shortfall in customer funds (Reuters, November 2022). Mt. Gox failed in 2014 after losing about 850,000 BTC (Wired, March 2014). Those events explain why investors ask, "is crypto insured?" The honest answer is: sometimes, but only when the loss fits a written policy.

Our view is narrower than the usual marketing line. Crypto insurance is not a promise that digital assets are safe like insured bank deposits. It is an operational-risk tool. Lyn Alden, founder of Lyn Alden Investment Strategy, often separates asset volatility from custody risk. That distinction is the key to this guide: insurance may help with the system holding your assets, but it does not protect the investment thesis itself.

The Custody-First Coverage Map

For this guide, we use a simple original framework: the Custody-First Coverage Map. Ask three questions in order. First, who controls the private key? Second, what event caused the loss? Third, does the policy name that event as covered? If the answer fails at any step, a payout is unlikely.

- Control: exchange, qualified custodian, fund, protocol or self-custody wallet.

- Event: external theft, employee crime, cyber incident, user mistake, scam, market loss or code exploit.

- Policy wording: covered event, excluded event, sub-limit, deductible and claims notice deadline.

A practical analogy is household insurance. A policy can cover theft after a break-in, but it will not refund a bad purchase or pay because the owner left valuables on the sidewalk. Crypto insurance works the same way. The trigger matters more than the label on the brochure.

Background: Why Crypto Insurance Emerged

Crypto began with a safety gap. Early users often left coins on lightly supervised exchanges. When a platform failed, customers had few practical remedies. There was no federal deposit guarantee for tokens, and blockchain transfers could not be reversed simply because the result was unfair.

From Exchange Hacks to Institutional Custody

The industry response was better custody. Cold storage means keeping private keys offline. Multi-signature approval means several authorized signatures are required before funds move. A third-party audit is an outside review of controls, balances or procedures. These practices gave insurers something they could inspect.

As professional investors entered the market, underwriters began writing policies for exchanges, funds, miners and custody firms. The policy language was not standard retail coverage. It focused on defined storage procedures, employee access controls, cyber events and physical security. Understanding how crypto rules apply in 2026 also matters because regulation shapes what insurers are willing to price.

The history points to one rule: where the asset sits determines whether meaningful coverage is available. That is why the rest of this guide moves from custody location to coverage decisions.

Why Crypto Insurance Matters in 2026

As of 2026, digital assets sit in more places than they did during the first exchange-hack era: retail exchange accounts, hardware wallets, spot bitcoin funds, company treasuries, lending protocols and professional custodians. Each location has a different risk profile and a different insurance market.

Crypto ownership has also become mainstream enough for protection gaps to affect ordinary households. Triple-A estimated global crypto ownership above 560 million people (Triple-A, 2025). At that scale, a phrase such as "insured custody" needs careful reading, because a shared platform policy may not equal full protection for each customer.

Three risks are often confused. Market risk is the chance that a token price falls. Insurance does not pay because bitcoin or ether declines. Custody risk is the chance that the place holding your asset is hacked, fails or loses keys. This is the main area where crypto insurance can help. Fraud risk is the chance that a person is tricked into authorizing a transfer. Many policies exclude that unless a specific social-engineering clause exists.

Vitalik Buterin, co-founder of Ethereum, has repeatedly emphasized self-custody and wallet security as user-level responsibilities in public education around Ethereum. That matters for insurance because the more control a user takes, the less a commercial custodian can insure on the user's behalf.

Is Crypto Insured? It Depends Where Your Assets Sit

Is crypto insured? Some crypto is insured, but only under specific custody and policy conditions. There is no blanket protection for every wallet, exchange account or token. The custody location decides whether crypto insurance is realistic.

- Exchange custody: an exchange may carry commercial crime or cyber coverage, but limits are usually shared and user-caused losses may be excluded.

- Qualified custody: regulated or institutional custody is the most likely place to find documented policy limits and clearer claims procedures.

- Self-custody: a hardware or software wallet gives you control, but lost keys, bad signatures and wrong-address transfers are usually uninsured.

- DeFi: decentralized finance runs through smart contracts, which are pieces of code that execute transactions automatically. Narrow cover products exist, but broad portfolio insurance does not.

- Investment products: funds and trusts depend on their own custodian, legal structure and disclosed insurance arrangements.

Exchange-Held Crypto

When you leave coins on a centralized exchange, the exchange controls the private keys. Some platforms disclose commercial insurance. Coinbase states that it carries crime insurance for a portion of assets held in hot storage, which means assets kept online for liquidity, according to its insurance disclosure (Coinbase, accessed May 2026).

That does not mean your whole balance is insured. A platform policy can have a shared limit, sub-limits for hot wallets and exclusions for customer account compromise. Ask whether customers are named beneficiaries, what the total policy limit is and what loss events are excluded.

Self-Custody Wallets

Self-custody means you control the private key. A hardware wallet is a small offline device used to store that key away from internet-connected computers. The benefit is independence from an exchange. The cost is that you absorb most user-error risk yourself.

If you lose a seed phrase, sign a malicious transaction or send funds to the wrong address, a standard custody policy will not step in. A seed phrase is the 12-word or 24-word recovery phrase that restores wallet access. For a deeper custody comparison, see hardware wallet vs exchange custody.

DeFi and Smart Contracts

DeFi, short for decentralized finance, uses smart contracts instead of a centralized company to move funds. Smart-contract risk is hard to insure because code can fail instantly, liquidity can move across chains and user permissions can be abused.

Exploit data shows the scale of the problem. DeFi losses exceeded $1.8 billion in 2023 (DefiLlama, accessed May 2026). Some on-chain cover products target particular protocol failures, but they are narrow, capacity-limited and subject to their own contract rules. They should be treated as specialized protection, not as a substitute for wallet hygiene.

What Crypto Insurance Covers — and What It Usually Does Not

Knowing that a platform has insurance is only the first step. The useful question is what event, storage method and claimant the policy actually covers.

Usually covered | Usually not covered |

|---|---|

Theft from approved cold-storage custody | Market losses or price volatility |

Employee crime and internal fraud | Scams, phishing or social engineering |

Certain cyber events against approved custody infrastructure | Lost or forgotten seed phrases |

Physical damage to insured mining equipment | Bad trades or user-initiated errors |

Some operational failures at documented custodians | Smart-contract exploits unless a specific rider applies |

Commonly Covered Risks

Commercial policies vary, but covered events often include theft from approved cold storage, employee dishonesty, external cyber intrusion into custody systems and physical loss affecting insured equipment. A policy may also include directors and officers liability, which covers certain legal claims against company leadership.

The word "approved" matters. If a custodian moves assets outside the agreed process, skips required approvals or uses an unlisted storage method, the insurer can dispute the claim. Crypto policies are written around procedures, not only outcomes.

Common Exclusions and Grey Areas

Common exclusions include price drops, investment losses, voluntary transfers to scammers, lost recovery phrases, sanctions issues and transactions initiated by an authorized account holder. If a user authorizes a malicious transaction, the blockchain may record it as valid even when the user was deceived.

DeFi exploits are a grey area. A Chainalysis report estimated that crypto hacking losses remained heavily concentrated in DeFi, with hundreds of millions of dollars stolen in 2024 (Chainalysis, 2024). Traditional custody policies often exclude code-level failures unless the buyer adds a specific endorsement.

Coverage Limits, Deductibles and Sub-Limits

A deductible is the amount the insured party pays before coverage responds. A policy limit is the maximum the insurer will pay. A sub-limit is a smaller cap inside the policy for a specific risk, such as hot-wallet theft.

This is where marketing language can mislead. A custodian may hold billions of dollars in assets while carrying insurance that covers only a portion. Brian Armstrong, co-founder and CEO of Coinbase, has discussed the practical difficulty of covering all customer assets at large crypto platforms. The takeaway is simple: the existence of a policy is not the same as full account-level protection.

How Crypto Insurance Works: Underwriting, Premiums and Claims

Crypto insurance follows the same basic path as other commercial insurance: underwriting, pricing, policy conditions and claims review. The difference is the evidence. Insurers need to understand cryptographic controls, wallet architecture, employee permissions and incident response.

Step 1: The Insurer Reviews the Security Stack

Underwriting means the insurer's review of risk before offering coverage. For crypto, the review may include multi-signature procedures, cold-storage design, access logs, background checks, audit reports, withdrawal controls and incident response plans. Multi-signature means more than one private key is required to approve a transaction.

For readers, this creates a useful signal. A custodian that can publish clear controls, audited procedures and policy summaries is easier to evaluate than a platform that says only "insured" without details.

Step 2: The Policy Sets Conditions

Coverage depends on conditions. A policy might require a fixed number of approvals for withdrawals, segregation of duties, specific storage locations or a notice deadline after an incident. If the insured firm breaks those conditions, the insurer may deny or reduce a claim.

That is why policy wording matters more than advertising. Look for the covered event, excluded events, deductible, total limit, sub-limits and whether customers have direct rights under the policy.

Step 3: A Claim Must Prove an Insured Loss

When a loss occurs, the insured party must prove that it fits the policy. A typical claims process includes:

- Report the event within the notice window stated in the policy.

- Preserve logs for systems, approvals, wallet access and employee actions.

- Document wallet addresses, transaction hashes and timestamps.

- Cooperate with investigators, including blockchain forensics teams where required.

- Match the event to policy wording and show that no exclusion applies.

Incomplete evidence slows claims. Clean records do not guarantee payment, but they make it easier to show that the loss was insured rather than excluded.

Coverage by Use Case: Exchanges, Custodians, NFTs, Mining and DeFi

Coverage availability changes by use case because insurers prefer risks they can inspect and measure. The more documented the storage and operations are, the more likely a policy can be priced.

Custodians and Exchanges

Custodians and exchanges are the most developed part of the market. Underwriters can review cold-storage percentages, key management, employee controls and audit records. Lloyd's market participants have supported digital-asset custody insurance since at least 2020 (Lloyd's, March 2020). The gap is capacity: limits may be far below total assets held.

Mining Operations

Mining is an industrial business. Miners use specialized computers to validate transactions and earn coins. Insurance can cover property damage, equipment breakdown, business interruption, cyber liability and general liability. It does not cover the market price of mined coins. If bitcoin falls after production, that is market risk, not an insured equipment loss.

NFTs and Digital Collectibles

An NFT is a non-fungible token, meaning a blockchain token intended to represent a unique item or right. Insurance questions include storage, theft, title disputes and valuation. The hardest issue is value. A token that sold at one price last year may not have the same buyer demand today.

DeFi Protocols and Smart-Contract Risk

DeFi coverage is narrow because the risks are code-based and fast-moving. A bug, manipulated price feed or unsafe wallet approval can move funds before a human review is possible. Some cover products focus on named protocols or named failure events, but exclusions are detailed and claims rules can be strict.

Use case | Insurance maturity | Typical coverage | Key gap |

|---|---|---|---|

Qualified custody | Most developed | Specie, crime and cyber | Limits below total assets |

Exchange accounts | Moderate to developed | Crime, cyber and liability | Shared limits and user exclusions |

Mining businesses | Moderate | Property and equipment | No price coverage |

NFTs | Early | Custody, theft and title | Valuation disputes |

DeFi | Limited | Named smart-contract events | Low capacity and exclusions |

How to Protect Your Portfolio Beyond Insurance

Crypto insurance is one layer in a risk plan. Your daily habits still matter because many common losses are excluded. If you send 0.5 BTC to the wrong address, the transaction can settle permanently within minutes. The bitcoin network passed 1 billion cumulative transactions by early 2026 (Bitcoin.org, accessed May 2026), and final settlement is part of how the system works.

A Beginner-Friendly Security Checklist

- Use a reputable, regulated exchange for small active balances and check whether it publishes custody and insurance disclosures.

- Enable multi-factor authentication with an authenticator app rather than SMS where possible.

- Back up your seed phrase offline in two separate physical locations, never in cloud storage or photos.

- Use a hardware wallet for long-term holdings and follow how to set up a Ledger wallet safely before moving large amounts.

- Set withdrawal allowlists so exchange withdrawals can go only to pre-approved addresses.

- Test with a small transaction first before sending a large transfer to any new address.

- Verify links before clicking and review the warning signs your wallet is compromised if something feels wrong.

- Revoke risky token approvals by following this guide to revoke risky token approvals.

- Review your custody split every quarter so trading funds, long-term holdings and DeFi positions are not all exposed to the same failure point.

When Self-Custody Makes Sense

Self-custody makes sense when the amount is large enough that exchange failure would hurt and the holder is willing to learn key management. It does not make sense when a person has no safe seed-phrase storage plan.

A practical middle ground is a two-bucket approach. Keep trading funds on a well-documented exchange. Move long-term holdings to a hardware wallet you control. Insurance may help with the first bucket. Your process protects the second. If a dispute does arise, understanding when to hire a crypto lawyer can help you preserve evidence and deadlines.

Balaji Srinivasan, author and investor and former CTO of Coinbase, has long framed crypto ownership as a shift toward user responsibility. That idea is useful here. Insurance can reduce some institutional risks, but it cannot replace careful custody decisions.

Frequently Asked Questions

- Is there any insurance for cryptocurrency?

- Yes, but coverage is limited. Cryptocurrency insurance typically applies to specific risks such as custody losses, crime and, in some cases, smart-contract failures. Most policies do not cover price declines, poor trading decisions or every customer balance held on a platform. Institutions generally have better access to these products than individual investors.

- Is stolen crypto recoverable?

- Sometimes. Stolen crypto can be traced on a public blockchain, but actually recovering it is difficult and rarely guaranteed. Recovery efforts may involve exchanges freezing funds, blockchain analytics firms, law enforcement and legal action. Insurance may cover the loss only if the theft matches the specific language written into your policy.

- Is any crypto FDIC insured?

- No. FDIC insurance protects eligible cash deposits held at insured banks — it does not extend to Bitcoin, Ether, stablecoins or digital asset balances held on exchanges. Even if a platform keeps some cash in an FDIC-insured bank, your actual crypto holdings remain outside that protection entirely.

- What is the safest way to protect my crypto?

- Layered security works best. Use reputable platforms, move long-term holdings to a hardware wallet, store your seed phrase offline and enable multi-factor authentication. Test small transfers before moving large amounts, avoid suspicious links and revoke unnecessary token approvals regularly. No single method eliminates all risk, so combine several practices.

- Can cryptocurrency be insured?

- Yes, under certain circumstances. Whether coverage applies depends on who holds the asset, how it is stored, what caused the loss and whether that event is listed in the policy. Institutional custodians typically have broader options. Self-custody mistakes, such as losing a seed phrase or signing a bad transaction, are commonly excluded.

- Can you get your money back if you get scammed on crypto?

- Refunds are uncommon because most blockchain transactions are irreversible. If you are scammed, document everything, contact the platform immediately and report the incident to law enforcement. Be cautious of recovery services that charge upfront fees — many are scams themselves. Standard insurance policies rarely cover voluntary transfers made to fraudsters.

- Will crypto ever be FDIC insured?

- It is unlikely without significant legal and regulatory changes, since FDIC insurance was built specifically for bank deposits. Future regulation could introduce new forms of digital asset protection, but as of 2026, no such framework exists. Investors should not assume that FDIC-style safeguards will apply to their crypto holdings anytime soon.

- Can I lose my crypto in a wallet?

- Yes. A wallet holds the private keys that control your crypto, not the assets themselves. Losing your seed phrase, sending funds to a wrong address, exposing your private key or signing a malicious transaction can all result in permanent loss. Insurance products rarely cover these types of basic user errors.

Sources

Author

Crypto analyst and blockchain educator with over 8 years of experience in the digital asset space. Former fintech consultant at a major Wall Street firm turned full-time crypto journalist. Specializes in DeFi, tokenomics, and blockchain technology. His writing breaks down complex cryptocurrency concepts into actionable insights for both beginners and seasoned investors.