Securities Law Crypto Guide: How SEC Rules Apply in 2026

Securities Law Crypto Guide: How SEC Rules Apply in 2026

Securities Law Crypto: The Plain-English Definition

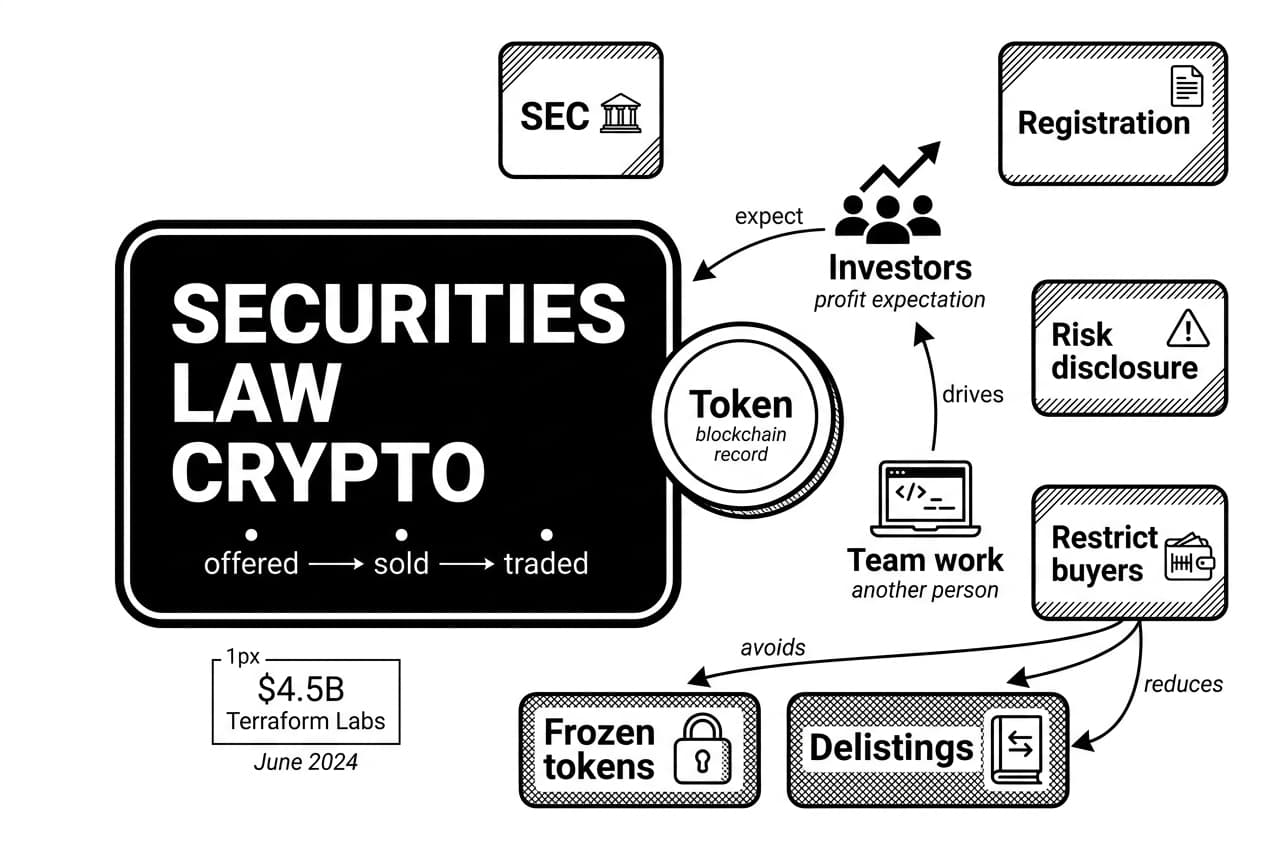

Securities law crypto means the rules that control how digital-asset investments are offered, sold, disclosed, and traded when a crypto transaction works like a regulated investment product and buyers expect profits mainly from another person or team's work.

Why It Matters

That definition affects real choices for token buyers, founders, exchanges, DeFi users, and developers. If a token sale is treated as a securities offering, the seller may need to register with the SEC, disclose financial and technical risks, restrict who can buy, and avoid profit promises. If a project ignores those duties, buyers can face frozen tokens or delistings, while founders and platforms can face refunds, penalties, or court orders.

A few terms help at the start. A security is an investment product regulated by law, such as a stock, bond, or investment contract. A token is a digital asset recorded on a blockchain. A blockchain is a shared database maintained by many computers instead of one central server. A wallet is software or hardware that stores the private keys used to control crypto. An issuer is the person or company that creates and sells a token. An investor is a buyer who expects financial gain. A regulator is a government agency that writes or enforces market rules.

Public records show why the stakes are not theoretical. The SEC announced a final judgment of about $4.5 billion against Terraform Labs and its founder (SEC, June 2024). In a separate staking case, Kraken agreed to stop its U.S. staking service and pay $30 million (SEC, February 2023). These cases show how marketing, yield promises, and investor reliance can turn a crypto product into a securities-law problem.

Why It Matters for Token Buyers, Founders, and Exchanges

Token buyers care because securities rules are designed to force honest disclosure before money changes hands. Founders care because fundraising, token vesting, treasury control, and marketing can all shape legal risk. Exchanges care because listing an unregistered security can raise separate broker, dealer, clearing, or exchange-registration questions. Developers care because writing open-source code is different from selling tokens to finance a team, but the line can blur when a small group controls upgrades and holds a large token allocation.

Hester Peirce, Commissioner at the U.S. SEC, has repeatedly argued in public statements that digital-asset projects need clearer rules before enforcement begins. Brian Armstrong, co-founder and CEO of Coinbase, has also pushed publicly for clearer U.S. rulemaking for crypto markets. Their positions differ in role and perspective, but both point to the same practical problem: projects often need to make design decisions before the law gives a clean answer.

A Practical Analogy: A Token Sale as a Startup Investment Pitch

A useful analogy is a startup pitch. A founder says: pay $500 today, we will build the app, and your tokens should become more valuable once users arrive. That is not just a sale of software access. It sounds like fundraising from people who expect profit from the founder's future work. Securities law was built to police that kind of investment pitch, even when the object sold is called a token instead of a share.

The better question is not simply whether a token is always a security or never a security. The transaction-first question is narrower: does this offer, sale, staking program, lending product, exchange listing, or intermediary relationship create an investment contract? The same token can appear in one legal context during a presale and in a different context years later on a working network.

- Securities law controls investment offerings, disclosures, trading, and anti-fraud duties.

- Crypto securities regulation focuses on facts: what was sold, who sold it, what was promised, and who buyers relied on.

- The token is not the whole answer. The offer and sale often matter more than the label on the asset.

- Risk can last. A token sold years earlier without proper compliance can still attract enforcement attention.

Background: Why Securities Law Reached Crypto

Securities law did not begin with Bitcoin. It began with investor losses and market fraud. After the 1929 stock market crash, U.S. lawmakers passed the Securities Act of 1933 and the Securities Exchange Act of 1934. The basic bargain was simple: if you raise money from the public by offering an investment, you must tell buyers the truth about the risks.

History: What the SEC Is Designed to Do

The SEC is the main U.S. federal securities regulator. Its work includes reviewing public-company disclosures, policing fraud, overseeing securities exchanges and broker-dealers, and enforcing rules for investment offerings. In plain English, the agency asks whether investors received enough accurate information before risking money.

Crypto reached securities law because many early projects sold tokens before a network or app existed. Buyers were not using the token yet. They were funding a future buildout and hoping the token price would rise. Between 2017 and 2018, projects raised more than $7.8 billion through initial coin offerings (CoinDesk, December 2018). That fundraising wave made token sales impossible for regulators to ignore.

From ICOs to Modern Digital Assets

Initial coin offerings were only the first fact pattern. By 2026, digital assets include several different structures:

- ICO and presale tokens: tokens sold before a product works, often to fund development.

- NFTs: unique digital items that may be art, memberships, game items, or fractional investment products depending on structure.

- Governance tokens: tokens that may give voting rights in a protocol, but can also trade for money.

- Staking products: arrangements where users lock tokens and may earn rewards.

- Lending products: arrangements where users deposit crypto so a platform can lend or invest it.

- Exchange-listed assets: tokens traded through intermediaries that may themselves face registration duties.

These categories share blockchain technology, but they do not share one legal answer. A collectible NFT, a pooled yield product, and a pre-launch token sale raise different securities law crypto questions.

The Howey Test: How Regulators Identify an Investment Contract

The Howey test is the U.S. legal test for deciding whether a deal is an investment contract, which is one type of security. It comes from a 1946 Supreme Court orange-grove decision (Justia, 1946). The test looks at economic reality, not labels. Calling a token a utility token does not end the analysis.

The Four Howey Factors in Simple Terms

Regulators and courts review these factors together. A transaction that meets all four is more likely to be treated as a securities transaction.

- Investment of money: A buyer gives money, crypto, services, or another thing of value.

- Common enterprise: The buyer's outcome is tied to the fortunes of a project, pool, or group.

- Expectation of profit: The buyer expects financial upside, such as price gains, yield, or rewards.

- Reliance on the efforts of others: The expected profit depends mainly on a team, operator, promoter, or manager.

Example: Alice pays $1,000 in USDC for tokens before a network launches. The whitepaper says the team will build the protocol, list the token, and grow demand. Alice has invested value, her outcome is tied to other buyers and the project, she expects profit, and the team's future work drives that profit. That transaction fits the investment-contract pattern.

Why the Asset and the Transaction Are Not Always the Same Thing

A token is a digital record. The legal question is often the deal wrapped around that record. A concert ticket is not normally a security. But if a promoter sold ticket packages by promising that the promoter's work would create resale profits for buyers, the package starts to look less like entertainment access and more like an investment arrangement.

The same logic applies to crypto. A token used today to pay gas fees on a working network can look different from the same token sold months earlier to fund development. Gas fees are transaction fees users pay to have blockchain transactions processed. Functional use matters, but it does not erase earlier fundraising facts.

Hester Peirce, Commissioner at the U.S. SEC, has argued that developers and network users should not automatically face the same treatment as promoters who originally sold tokens to investors. That distinction is central to the transaction-first approach in this guide.

Where the Howey Test Can Be Hard to Apply

The test is simple to state and hard to apply in several crypto settings:

- Decentralized networks: If no small team controls upgrades, treasury decisions, or promotion, reliance on others may be weaker.

- Secondary-market trades: A buyer on an exchange may not be funding the original issuer or hearing a direct profit promise.

- Airdrops: Free tokens may lack a money payment, but referrals, labor, or data can still count as value in some arguments.

- Staking rewards: Rewards can come from protocol mechanics, an intermediary's management, or a mix of both.

- Open-source work: Code contributions are not the same as securities sales, but token allocations and promotional activity can change the facts.

The transaction-first decision tree for 2026 asks four practical questions before debating labels: who received value, what did buyers expect, whose work created the expected profit, and what disclosures were given before the sale?

When Crypto Assets May Trigger Securities Laws

Knowing the Howey test in theory is not enough. The practical task is spotting the fact patterns that trigger securities law crypto risk. Regulators focus on substance. If a sale funds a team, promises upside, and leaves buyers dependent on that team, legal risk rises.

Token Sales, Presales, and Fundraising Rounds

Presales are high-risk because buyers often have no live product to use. They are funding a roadmap. A roadmap is a project's public plan for future features, launches, or listings. If the roadmap is marketed as the reason a token will rise in price, the sale starts to resemble an investment offering.

Simple agreements for future tokens, private rounds, public presales, and initial coin offerings can all raise securities issues. The label matters less than the economics. If 5,000 buyers each send $200 to a project because the team says a network launch will increase token value, regulators will ask whether those buyers relied on the team to create profit.

Staking, Lending, and Yield Products

Staking means locking tokens to help secure a proof-of-stake blockchain or to receive rewards. Lending means depositing crypto so someone else can borrow or invest it. A direct protocol reward may raise different issues from a custodial product where a company pools funds, controls strategy, and advertises yield.

The Kraken order is a clear dated example. The SEC said Kraken's staking-as-a-service program offered an investment contract, and Kraken agreed to pay $30 million (SEC, February 2023). The lesson is not that every staking action is a security. The lesson is that pooling, custody, managerial control, and yield marketing can change the legal analysis.

Secondary-Market Trading and Exchange Listings

A secondary-market trade happens when a buyer purchases a token from another holder instead of from the original issuer. These trades can involve different facts because the buyer may not be funding the development team. Even so, platforms that list tokens face their own questions. If a platform handles trades in securities, it may need to register or qualify for an exemption.

The table below is a quick reference, not legal advice. Real answers depend on the facts and the jurisdiction.

More likely to raise securities-law issues | Less likely, depending on facts |

|---|---|

Presale before network launch with profit-focused marketing | Token sold after a working network has real users |

Yield product where an operator controls returns and custody | Protocol-level staking without a manager pooling customer funds |

Token promoted with return projections, price targets, or exchange-listing hype | Token used immediately for access, fees, or in-app functions |

Small team controls upgrades, treasury, supply, and marketing | Broad network participation with no dominant control group |

Exchange listing after a regulator has alleged the asset was sold as a security | Trading of assets with clearer commodity treatment on a properly registered or compliant platform |

What SEC Oversight Means in Practice

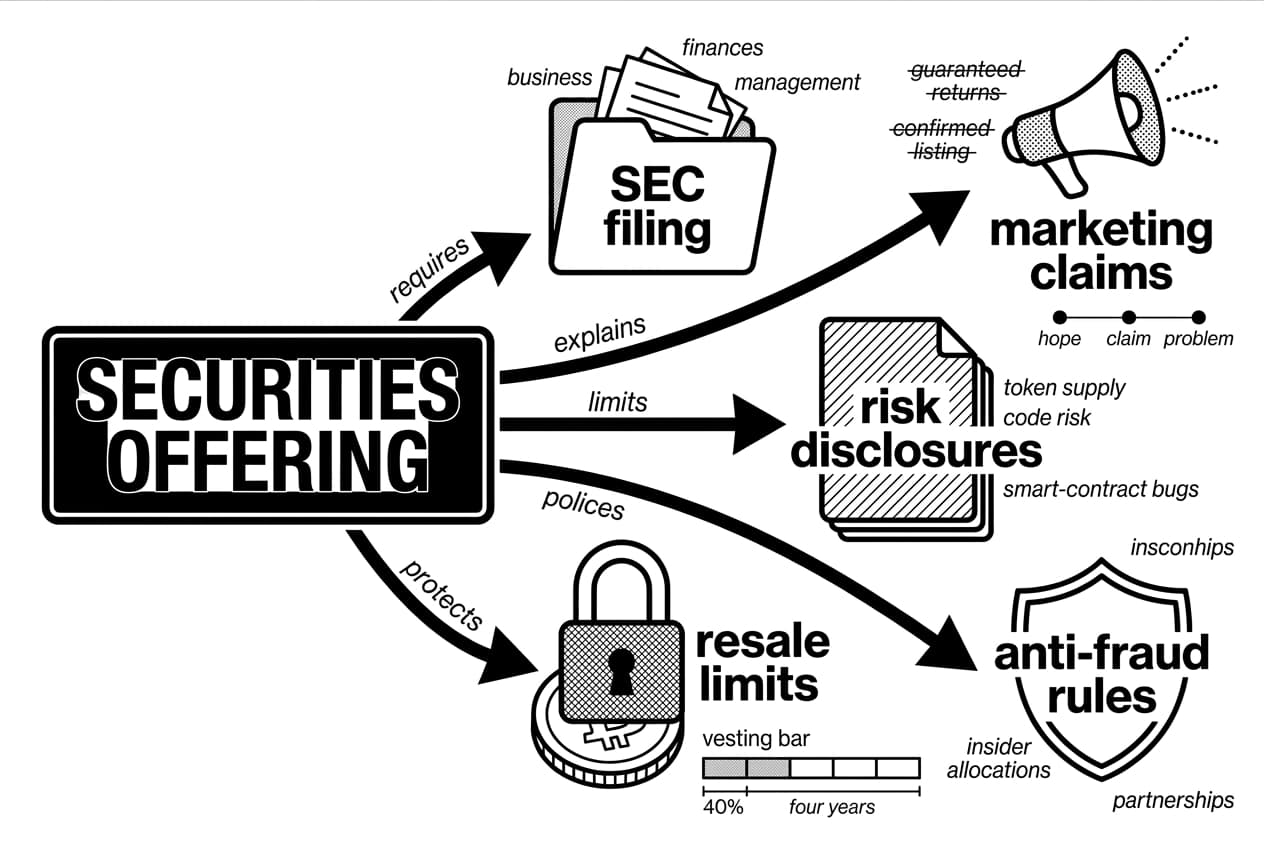

When a crypto transaction is treated as a securities offering, the rules become concrete. The issuer may need to register, give risk disclosures, limit resale, monitor marketing, and follow anti-fraud rules. Buyers may gain legal protections, but they can also face restricted liquidity if the offering was not handled correctly.

Registration and Disclosures

Registration means filing detailed offering documents with the SEC before selling securities to the public. Those documents typically explain the business, finances, management, token supply, conflicts of interest, and risks. For a token project, disclosures may also cover code risk, smart-contract bugs, treasury control, vesting, governance, and liquidity.

Token vesting contracts deserve special attention because they affect when insiders can sell. If insiders receive 40% of a token supply but open up over four years, buyers need to understand that schedule before making an investment decision.

Anti-Fraud Rules and Marketing Claims

An exemption from full registration is not permission to mislead. Anti-fraud rules still apply. A project should not overstate partnerships, hide insider allocations, imply guaranteed returns, or claim an exchange listing is confirmed when it is only a hope.

Example: a project raises $20 million from U.S. buyers while saying a major exchange listing is already secured. If no signed agreement exists, that statement can become a securities-fraud problem even if the project believed a listing was likely. The safer rule is plain: say what is true, label uncertainty clearly, and keep records showing why each claim was accurate when made.

Enforcement Actions and Precedents

Enforcement data gives a practical read on regulator priorities. The SEC brought 46 cryptocurrency-related enforcement actions in 2023 (Cornerstone Research, January 2024). Those actions commonly involved unregistered offerings, fraud claims, exchange or broker questions, staking products, lending products, and misleading promotion.

The main lessons are direct. U.S. investor participation can create U.S. exposure even if a project forms offshore. Secondary trading can create platform risk even when the original sale happened earlier. Founders, executives, promoters, and platforms can face personal or entity-level liability depending on their role.

Hester Peirce, Commissioner at the U.S. SEC, has criticized enforcement-first policy because it can punish projects before they receive workable compliance instructions. For a founder, that means securities analysis should happen before launch, before marketing, and before exchange-listing outreach.

Registration Exemptions and Compliance Paths

Not every securities offering requires a full public registration, but skipping registration is not the same as skipping compliance. Exemptions are legal pathways with conditions. A project that misses those conditions can lose the exemption.

Common Exemption Concepts for Crypto Projects

Regulation D is often used for private placements to accredited investors. An accredited investor is usually a person or entity that meets wealth, income, or professional criteria. For individuals, common thresholds include net worth over $1 million excluding a primary residence or income over $200,000 in each of the two most recent years (SEC, accessed March 2026). Tokens sold under private-placement rules often have resale restrictions.

Regulation S can apply to offshore offers and sales outside the U.S., but it does not allow a project to quietly route tokens back to U.S. buyers. Regulation Crowdfunding permits smaller public raises with strict limits and platform rules. The annual Reg CF cap is $5 million (SEC, March 2021 framework update). Regulation A can allow a broader offering, but it requires SEC review and detailed disclosures.

These paths can affect token design. Vesting, transfer limits, investor eligibility, exchange plans, and marketing language should match the exemption. A mismatch can turn a fundraising shortcut into an enforcement risk.

Compliance Checklist for Businesses

This is educational information, not legal advice. Before launching a sale, founders should review when to hire a crypto lawyer and apply the checklist to their specific facts.

- Identify jurisdictions. List where buyers, founders, servers, entities, and marketing channels are located.

- Analyze the factors under Howey. Document value paid, common enterprise facts, profit expectations, and reliance on a team or operator.

- Choose registration or exemption. Compare public registration, Reg D, Reg S, Reg CF, Reg A, or a non-security design.

- Prepare disclosures. Explain treasury use, token supply, insider allocations, technical risk, legal risk, and liquidity limits in plain language.

- Review marketing. Remove price targets, guaranteed-return language, vague partnership claims, and listing hype.

- Consult counsel. Have qualified securities counsel review offering documents, token mechanics, resale limits, and platform plans.

The 2026 Regulatory Picture: SEC, Courts, Congress, and the World

As of March 2026, the U.S. rule set remains partly built through enforcement, court decisions, agency guidance, and proposed legislation. That mix is why beginners see conflicting claims online. One source may focus on court rulings about secondary sales. Another may focus on enforcement orders about staking or lending. Both can be true in different contexts.

What Has Changed by 2026

Several developments shape crypto securities regulation in 2026. The House passed FIT21 by a vote of 279 to 136 (Office of the Clerk, May 2024), showing bipartisan interest in clearer market-structure rules even though final U.S. legislation still depends on the full lawmaking process. The SEC's prior enforcement-heavy period is reviewed in our SEC term analysis. Outside the U.S., the EU's MiCA rules applied to stablecoin issuers from June 30, 2024 and to other crypto-asset service providers from December 30, 2024 (European Commission, 2024).

Regional approaches differ. For comparison, see our guides to crypto regulation in mexico, argentina, and colombia and crypto regulation in africa. The main point for readers is that securities analysis is local as well as factual. A product can face one rule set in the U.S., another in the EU, and another in a market where it is promoted or listed.

Looking Ahead

The likely direction is more classification, not less oversight. Lawmakers and regulators are trying to separate payment tokens, commodities, securities, stablecoins, tokenized stocks, tokenized bonds, and DeFi interfaces. The hard questions for 2026 are practical:

- Secondary trading: When does resale on an exchange create duties for the seller or platform?

- DeFi front ends: Can a website that connects users to a protocol be treated as a broker or exchange?

- Staking: When is staking a protocol function, and when is it a managed investment product?

- Stablecoins: Should dollar-pegged tokens be governed by banking rules, securities rules, payment rules, or a new statute?

- Tokenized real-world assets: A tokenized stock or bond is still likely a security, even if it settles on a blockchain.

The practical approach is to build records before risk appears. Save marketing drafts, document design decisions, record who controls upgrades, and track why buyers would purchase the token. Those facts are the evidence regulators and courts examine later.

Key Takeaways

What Readers Should Remember

Securities law crypto analysis becomes easier when you separate the asset from the transaction. Ask what was sold, how it was marketed, who buyers relied on, and what disclosures were given.

- The transaction usually matters more than the label. A token is not automatically a security, but a sale of that token can be a securities offering.

- The Howey test is the core U.S. tool. It asks whether buyers invested value in a common enterprise with expected profit from others' efforts.

- Marketing can create risk. Price targets, yield promises, listing hype, and team-controlled roadmaps can all support securities arguments.

- Compliance paths exist. Registration, Reg D, Reg S, Reg CF, and Reg A can work only if their conditions are followed.

- Check before launch. Founders, exchanges, and developers should review crypto securities regulation before selling, listing, or promoting a token.

Frequently Asked Questions

- What is the SEC ruling on crypto?

- There is no single SEC ruling that covers all cryptocurrency. The SEC's position has developed through guidance documents, enforcement actions, settlements, and court decisions. Whether a specific crypto asset qualifies as a security typically depends on whether it meets the Howey Test criteria for an investment contract.

- Is XRP considered a security by the SEC?

- XRP sits at the center of ongoing SEC litigation, and the answer depends heavily on context. Courts have distinguished between institutional sales of XRP and other types of market transactions, reaching different conclusions for each. No blanket ruling declares every XRP transaction a security or definitively clears all of them.

- What is Trump's new crypto law?

- As of 2026, several executive orders and legislative proposals have reshaped crypto policy, including efforts to clarify CFTC and SEC jurisdictional boundaries and establish stablecoin frameworks. Specific enacted statutes vary from broader proposals and campaign statements, so confirming whether a particular measure became law before relying on it is important.

- Can my wife take my crypto in a divorce?

- This is a family law question, not a securities law issue. Crypto can be treated as marital property depending on your jurisdiction, when you acquired it, and how it was held. Exchange account records, wallet addresses, and tax filings all matter. Consulting a divorce attorney and a financial forensics expert is strongly advisable.

Sources

Author

Crypto analyst and blockchain educator with over 8 years of experience in the digital asset space. Former fintech consultant at a major Wall Street firm turned full-time crypto journalist. Specializes in DeFi, tokenomics, and blockchain technology. His writing breaks down complex cryptocurrency concepts into actionable insights for both beginners and seasoned investors.