Crypto Regulation Africa: Nigeria, Kenya, South Africa 2026

Crypto Regulation Africa: A Plain-English Overview

Crypto regulation in Africa means the laws, licensing rules, tax requirements and anti-money-laundering controls that decide how people and companies may legally use digital assets, run exchanges, keep customer records, report suspicious activity and pay tax when crypto is bought, sold, swapped or used for payment.

Why it matters: if you want to buy Bitcoin through a local app, accept stablecoin payments from overseas clients, build a Web3 product or file taxes correctly, the written law is only one part of the answer. Bank access, identity checks, exchange licensing and tax reporting decide what you can actually do in Nigeria, Kenya and South Africa in 2026.

Plain definition: a blockchain is a shared digital record of transactions. Think of a blockchain like a shared spreadsheet that nobody can quietly edit after saving. A wallet is the app or device that holds your private keys, meaning the passwords that control your crypto. A virtual asset service provider, often shortened to VASP, is a business such as an exchange, broker or custodian.

The common story says African crypto policy is moving from bans to friendly rules. The more useful reading is narrower: legal clarity is improving, but payment rails still decide daily access. A country can allow licensed crypto firms on paper while banks, card processors and mobile-money partners still refuse them in practice.

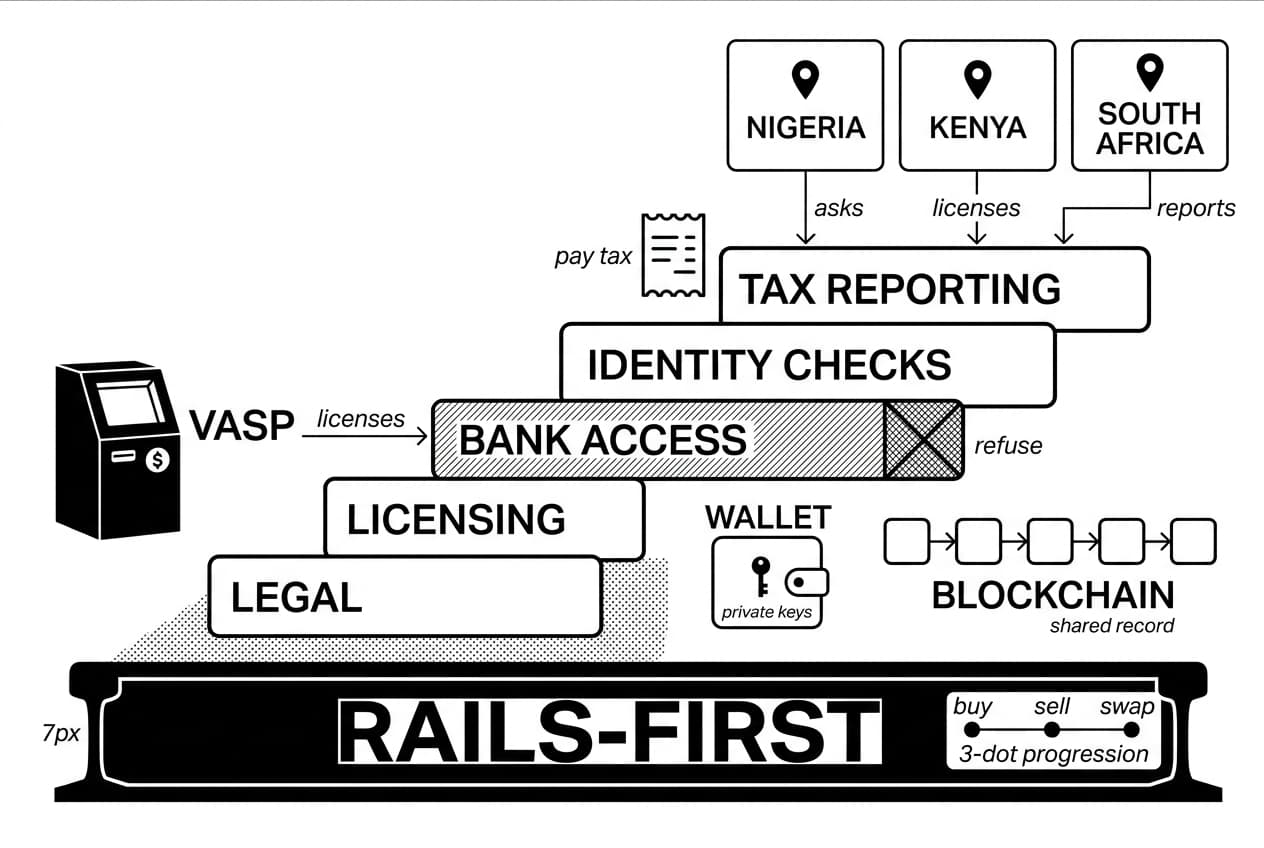

This guide uses a Rails-first compliance framework: first ask whether crypto is legal, second ask who licenses platforms, third ask whether local banks support deposits and withdrawals, and fourth ask what tax and anti-money-laundering records must be kept. That order reflects how users and exchanges actually operate.

- Crypto regulation africa is not one rulebook. Each country has its own agencies and timelines.

- Nigeria crypto regulation now combines securities licensing, central-bank banking rules and tax duties.

- South Africa crypto rules are the most formal of the three, with licensing and financial-crime controls already active.

- Kenya has taxed digital assets while its full VASP licensing law continues to develop.

- Bank access may matter more than a headline saying crypto is legal.

Background: Why African Crypto Rules Are Accelerating in 2026

Crypto rules across Africa are moving faster because governments are responding to adoption, fraud, cross-border payments and international anti-money-laundering reviews. The pressure is economic as much as political.

The economics driving crypto adoption in Africa

Remittances, freelance payments and trade settlement are major drivers. The World Bank recorded an average remittance cost of more than 6% globally and higher costs in many African corridors, with pricing data published through the World Bank remittance prices database, Q1 2026. When a worker sends money home every month, a two-point fee difference can matter more than a debate about blockchain theory.

Kenya shows why digital money feels familiar to many users. M-Pesa processed more than 36 trillion Kenyan shillings in transactions during the 2023/24 financial year, according to Safaricom, 2024. That does not mean crypto and mobile money are the same. It means regulators are dealing with a public that already expects phone-based payments to work quickly.

Nigeria adds a currency-pressure story. When local currency loses buying power, some users turn to dollar-pegged stablecoins, which are tokens designed to track the value of the US dollar. Similar forces are also shaping crypto regulation in Latin America, where inflation, remittances and payment rails also drive adoption.

The role of FATF, AML and the Travel Rule

FATF means the financial action task force, the global standard setter for controls against money laundering and terrorist financing. AML means anti-money-laundering controls. The Travel Rule is a FATF rule that requires certain crypto service providers to collect and share sender and recipient information when transfers meet the local reporting threshold.

Nigeria was placed on the FATF grey list in February 2023, according to the FATF country page for Nigeria, 2023. Grey-listing signals that a country must improve financial-crime controls. That pressure helps explain why crypto licensing and reporting duties moved up the policy agenda.

Two approved industry voices help frame the policy debate, even though local law must always come from local regulators. Brian Armstrong, co-founder and chief executive of Coinbase, has often linked regulatory clarity with bank access and institutional participation. Hester Peirce, commissioner at the US Securities and Exchange Commission, is widely associated with the view that clear rules are better than regulation by enforcement. For Africa, the hard question is whether clarity reaches banks and users, not only statute books.

- Payment costs make crypto attractive for some remittance and freelance-payment use cases.

- Mobile-money habits make phone-based financial tools easier to understand, especially in Kenya.

- Stablecoins are often used for dollar exposure, not only speculation.

- FATF pressure is pushing governments toward stricter licensing and reporting.

- Local variation matters. Lagos, Nairobi and Johannesburg do not share one compliance process.

Nigeria Crypto Regulation: From Banking Ban to Licensing Rules

Nigeria crypto regulation has shifted from bank restrictions to supervised access. Owning crypto was not the same as running a licensed exchange, and that distinction remains important in 2026.

A brief history of Nigeria's crypto policy

In February 2021, the central bank of Nigeria directed regulated banks to close accounts linked to crypto businesses and stop processing crypto-related transactions. The measure restricted access to banking rails rather than criminalising every private holder of crypto.

In December 2023, the central bank changed course and issued guidance allowing banks to serve crypto businesses that meet regulatory conditions. The securities regulator later used an accelerated incubation route for virtual asset businesses. As of May 2026, a user should treat Nigerian crypto as permitted only when the platform, payment route and tax records all line up.

A major enforcement signal arrived in 2024 when Nigerian authorities pursued Binance over registration, tax and market-conduct concerns. Reuters reported the enforcement dispute in February 2024. The lesson for exchanges is direct: registration risk in Nigeria can become an operational and personal-liability issue, not just a fine.

What Nigerian users and exchanges should check in 2026

- Licensing status: confirm whether the platform has approval from Nigeria's securities regulator or is operating through an official regulatory route.

- Bank deposit support: check whether your own bank permits transfers to and from the platform. A national policy change does not force every bank to approve every crypto flow.

- KYC: know-your-customer checks mean identity verification, usually including an official ID, address details and sometimes source-of-funds information.

- Tax records: keep trade dates, naira values, fees and wallet addresses. Existing income-tax and capital-gains principles can apply even where a crypto-specific tax form is not available.

- Peer-to-peer risk: P2P trading may be popular, but fraud, frozen bank accounts and suspicious-transaction reporting can create real problems.

The practical bottom line is that Nigeria has moved beyond the 2021 bank-access freeze, but users should still prefer registered platforms, clear bank rails and downloadable records.

- 2021: banks were told to stop servicing crypto-related accounts.

- December 2023: supervised bank access became possible for compliant operators.

- 2024: high-profile enforcement against a global exchange showed that registration matters.

- 2026 watch item: full VASP licensing, bank policy updates and tax reporting practice.

Kenya: Tax-Led Oversight and the Path to VASP Licensing

Kenya has moved first through taxation and consultation, rather than a finished licensing regime. That creates a simple but awkward result: tax duties can exist before every platform-licensing question is settled.

Why mobile money shapes Kenya's crypto debate

Kenya's mobile-money system gives regulators a clear benchmark for consumer protection. If millions of users can send shillings by phone, any crypto product connected to local payment rails must answer familiar questions: who holds customer funds, who reverses fraud, who reports suspicious transfers and who handles customer complaints?

The 36 trillion Kenyan shilling M-Pesa transaction figure from Safaricom, 2024 explains why payment regulators pay close attention. Crypto is not being assessed in isolation. It is being judged against a mature domestic payment system that users already trust.

Taxes, reporting and licensing signals

Kenya introduced a 3% digital asset tax on transfers or exchanges of digital assets through its 2023 finance law, with implementation referenced by the Kenya revenue authority, 2023. The rule is important because it shows the state can demand reporting even while the VASP licensing path is still being drafted.

As of May 2026, Kenya's full VASP licensing regime was still developing. The capital-markets regulator and payment authorities remain central to the debate, but users should not read the absence of a final licence category as an absence of legal duties.

- Main issue: tax and reporting duties are clearer than long-term licensing requirements.

- Tax rule: 3% digital asset tax was introduced in 2023.

- Payment concern: integration with mobile money and banks remains sensitive.

- User action: keep shilling-value records for every transfer, sale, swap and fee.

- Builder action: design for future licensing rather than assuming a permanent gap.

South Africa Crypto Rules: FSCA Licensing, FIC and the Travel Rule

South Africa crypto rules are the most structured of the three markets covered here. The country treats crypto asset services through financial-sector licensing, financial-crime reporting and tax disclosure.

What is a CASP in South Africa?

A CASP is a crypto asset service provider. It can include an exchange, custodian, broker or platform that arranges crypto services for customers. South Africa's financial-sector conduct regulator declared crypto assets to be financial products in October 2022, which brought many crypto businesses into the existing financial-advice and intermediary-services licensing system.

The regulator opened the licensing window in 2023 and later reported major industry take-up. It said it had received more than 300 CASP licence applications, according to the financial-sector conduct authority, 2024. It also reported 59 approved crypto asset service providers by March 2024, according to the same financial-sector conduct authority update, 2024.

FIC, FICA and AML duties explained simply

The FIC is South Africa's financial-crime agency. FICA is the law that requires accountable institutions to identify customers, keep records and report suspicious activity. For crypto platforms, this means identity checks before onboarding, transaction monitoring, record retention and suspicious-transaction reports when activity looks unusual.

A gas fee is the network fee paid to process a blockchain transaction. An on-chain transaction is a transfer recorded on the public blockchain. A licensed South African platform must often record both the blockchain details and the customer identity details behind the account.

How South Africa's crypto Travel Rule affects transfers

Yes, you may pay tax on crypto in South Africa. SARS can treat gains as income or capital gains depending on your activity. You should report sales, swaps, spending and crypto income, keep rand values at the transaction time, and retain records in case SARS asks for supporting evidence.

Recordkeeping examples are simple. If you sell 0.2 BTC, record the date, rand proceeds, cost, exchange fee and wallet or account used. If you swap ether for a stablecoin, record the rand value of both sides. If you receive freelance income in crypto, record the rand value when received.

The Travel Rule adds a data layer to certain transfers between regulated platforms. When a qualifying transfer moves from one licensed exchange to another, sender and recipient details may need to move with the payment information. This resembles bank-wire compliance, but it is applied to crypto transfers.

- CASP licence: required for many crypto exchange, custody and brokerage services.

- FICA duties: customer checks, records and suspicious-activity reporting apply.

- Travel Rule: identity data can be required for qualifying transfers.

- Tax: SARS expects crypto disposals and income to be reported.

- 2026 position: South Africa has the clearest framework among the three countries in this guide.

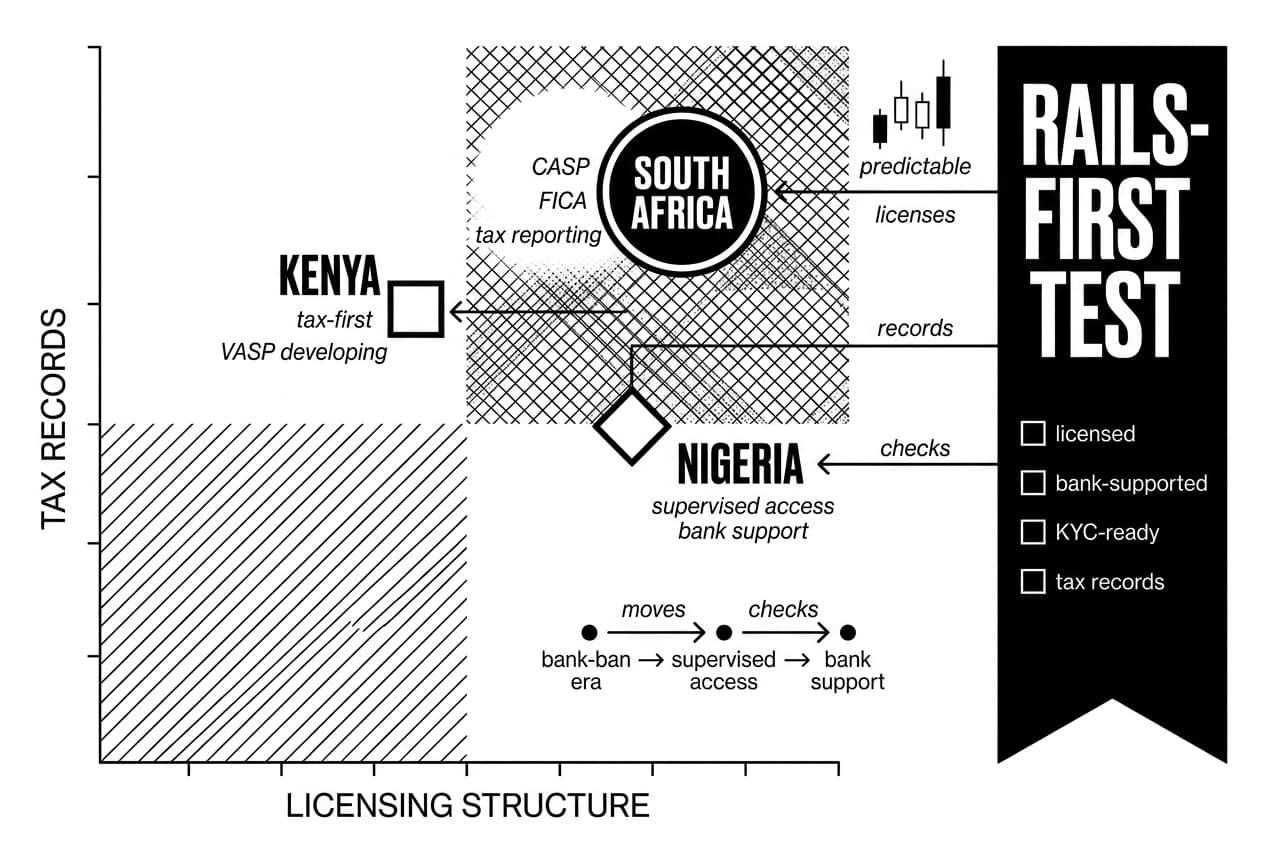

Nigeria vs Kenya vs South Africa: Side-by-Side Comparison

The table compares the three markets as of May 2026. It is a practical compliance snapshot, not legal advice.

Category | Nigeria | Kenya | South Africa |

|---|---|---|---|

Legal status | Permitted with supervised service-provider access | Permitted or tolerated, with tax duties active | Permitted under financial-sector rules |

Main regulator | Securities regulator, central bank and tax authority | Tax authority, payment regulator and capital-markets regulator | Financial-sector conduct regulator, FIC and SARS |

Licensing | VASP route required for platforms | Full VASP regime still developing | CASP licence required for covered services |

Tax | Income and capital-gains principles can apply | 3% digital asset tax introduced in 2023 | Income tax or capital gains tax depending on facts |

AML rules | Financial-crime reporting applies to regulated operators | General AML law applies; VASP-specific rules developing | FICA obligations apply to covered crypto providers |

2026 watch item | Full licensing rollout and bank adoption | Final VASP law and exchange reporting | Ongoing CASP supervision and Travel Rule practice |

Our 2026 rails-first compliance scorecard

The dataset below scores each country from 0 to 2 on five practical factors: legal status, licensing clarity, tax clarity, AML clarity and bank-rail predictability. Scores are editorial assessments based on official regulator publications and dated source material cited in this article.

Country | Legal status | Licensing clarity | Tax clarity | AML clarity | Bank rails | Total /10 |

|---|---|---|---|---|---|---|

Nigeria | 2 | 1 | 1 | 1 | 1 | 6 |

Kenya | 1 | 0 | 2 | 1 | 1 | 5 |

South Africa | 2 | 2 | 2 | 2 | 1 | 9 |

The scorecard supports the contrarian point of this article. South Africa is ahead because licensing and AML rules are clearer. Nigeria is moving quickly, but bank access and enforcement timing still matter. Kenya has tax clarity but less licensing certainty for businesses.

What the Rules Mean for Users, Exchanges and Web3 Builders

Rules matter only when translated into actions. The checks below apply whether you are buying your first crypto, running an exchange or building a Web3 product. Web3 means internet services that use blockchain networks for assets, identity, payments or governance.

What to check before using a crypto platform in Africa

- Licensing: is the platform registered or approved in the country where you live?

- KYC: does it verify identity before allowing deposits, withdrawals and high-value activity?

- Bank support: can you deposit and withdraw through a local bank or payment partner without workarounds?

- Fees: are trading fees, withdrawal fees, spreads and gas fees shown before you transact?

- Tax records: can you download transaction history with dates, values, fees and asset names?

For everyday users

Start with licensing and records. A platform with clear registration, local support and downloadable tax reports is usually safer than a platform offering only low fees. If you hold your own private keys, read the difference between custodial vs non-custodial crypto wallets. If you suspect a wallet problem, use this guide on how to check if your wallet is compromised.

For exchanges and Web3 startups

Compliance costs money, but it also opens bank accounts, payment partnerships and investor conversations. This is where the public comments of Brian Armstrong, co-founder and chief executive of Coinbase, are relevant: in regulated markets, clarity can make it easier for serious firms to build relationships with banks and institutions.

Use the three-part operating stack: first licensing, second AML and transaction monitoring, third customer disclosures and tax reporting. Do not wait until user growth forces a rushed repair.

Compliance area | Nigeria | Kenya | South Africa |

|---|---|---|---|

Primary permission | VASP approval route | Developing VASP regime | CASP licence |

Transaction monitoring | Required for regulated operators | Required under general AML duties | Required under FICA |

Customer disclosures | Expected for licensed services | Developing | Required for regulated services |

Data privacy | Local privacy law applies | Local privacy law applies | POPIA applies |

Bank relationships | Improving but uneven | Cautious | More predictable for licensed firms |

- Users: verify the platform, complete KYC and keep tax records.

- Exchanges: budget for licensing, monitoring, reporting and local counsel.

- Builders: design products around bank access and identity checks from day one.

Risks, Gaps and Africa's Digital Asset Future

The main risk in 2026 is not that African crypto has no rules. The bigger risk is that written rules, bank access and enforcement practice move at different speeds.

Why clear laws do not automatically mean easy access

A regulator can permit licensed crypto businesses while banks still decline accounts because of internal risk policies. This last-mile access problem affects users who need deposits and withdrawals, exchanges that need settlement accounts, and startups that need payment partners.

Several gaps deserve attention:

- Bank de-risking: local banks may avoid crypto even when regulators allow licensed activity.

- Pending applications: South Africa had more than 300 CASP licence applications reported by the financial-sector conduct authority, 2024, so supervision remains an ongoing process.

- Fraud pressure: cross-border scam activity keeps consumer protection high on the policy agenda.

- Tax reporting gaps: tax rules may arrive before exchanges have automated reporting tools.

- Privacy tension: Travel Rule data sharing must be reconciled with data-protection duties.

What's actually coming next

Stablecoins will stay central because they solve a direct problem: access to dollar-denominated value for trade, savings and freelance income. Regulators are likely to treat stablecoin issuers, reserves and redemption rights as separate topics rather than folding every token into one category.

Central bank digital currency policy also remains active. Nigeria's eNaira launched in 2021, and adoption has been slower than policymakers hoped. The Bank for International Settlements discussed low early usage, including figures below 0.5% of the population, in BIS research, 2023. For wider context, see this guide to CBDC policy developments.

Tokenized real-world assets may be another growth area if custody, investor-protection and secondary-market rules become clearer. For a related primer, see tokenized real-world assets. Cross-border settlement pilots also remain attractive because African remittance and payment corridors still carry high costs, with the World Bank remittance prices database, Q1 2026 showing fees that remain expensive for many users.

Key Takeaways

- Legal permission is not the same as practical access. Banks and payment partners still shape what users can do.

- Enforcement lags rulemaking. A new law can take months or years to become a smooth process.

- Travel Rule compliance creates data duties. Platforms must balance financial-crime reporting with privacy law.

- Stablecoins, CBDCs and tokenized assets are the next policy fronts in these markets.

Key Takeaways

After reading this guide, here is the short version of crypto regulation africa in 2026:

- Africa does not have one crypto rulebook. Nigeria, Kenya and South Africa use different regulators, tax rules and licensing timelines.

- Nigeria has moved beyond the bank-ban era. Supervised access is possible, but licensing and bank support must be checked carefully.

- Kenya is tax-first. Users should keep records now while the full VASP licensing framework develops.

- South Africa has the clearest structure. CASP licensing, FICA duties and tax reporting give it the most predictable framework of the three.

- The best practical test is rails-first. Ask whether the platform is licensed, bank-supported, KYC-ready and able to produce tax records.

Frequently Asked Questions

- Is crypto legal in Africa?

- There is no single Africa-wide crypto law. In many countries, including Nigeria, Kenya and South Africa, owning crypto is legal or tolerated, but rules vary sharply by jurisdiction. Trading on exchanges, paying taxes and operating a crypto business each carry separate legal considerations that differ from country to country.

- Which African countries are crypto friendly?

- South Africa offers some of the clearest regulatory structure, with FSCA licensing and AML requirements in place. Nigeria and Kenya have high adoption rates and developing frameworks. No African market is risk-free, but regulatory clarity, exchange availability and banking support vary considerably across these three countries.

- Is crypto now legalised in Nigeria?

- Nigeria has moved beyond a straightforward banking restriction toward a framework where compliant providers can operate under SEC oversight. However, users should verify exchange registration status, confirm current banking access, understand their tax obligations and stay updated on Central Bank of Nigeria guidance as of 2026.

- Is crypto regulated in Nigeria?

- Yes. Nigeria's Securities and Exchange Commission, the Central Bank of Nigeria and other authorities each play a role. Personal crypto ownership, running an exchange, accessing banking services and meeting anti-money-laundering requirements are treated as separate matters, each with its own rules and compliance obligations.

- Has Nigeria lifted the ban on crypto?

- Nigeria's earlier restriction targeted banks handling crypto-related accounts rather than banning individual ownership outright. Subsequent guidance allowed regulated financial institutions to work with virtual asset service providers that meet specific compliance conditions, marking a significant shift away from blanket exclusion toward supervised access.

- Why did Nigeria ban cryptocurrency?

- Nigerian authorities cited fraud, money laundering, capital flight, consumer protection and financial stability as primary concerns. At the same time, strong public demand for digital payments made an outright ban unsustainable, pushing policymakers to develop a regulated framework rather than continue relying solely on restrictions.

- Is Binance still banned in Nigeria?

- Access to specific exchanges, including Binance, can change due to licensing disputes, tax enforcement actions or consumer-protection concerns. The situation was evolving as of early 2026, so users should check the latest official statements from both the exchange and Nigerian regulators before attempting to use the platform.

- Do I pay tax on crypto in South Africa?

- South African taxpayers may owe income tax or capital gains tax on crypto activity, depending on whether SARS treats it as revenue or capital in nature. Keep detailed records of every purchase, sale, swap and receipt of crypto income, and consult a qualified tax professional for advice specific to your situation.

- Which crypto platform is best in South Africa?

- Rather than ranking platforms, prioritise FSCA licensing status, security practices, rand deposit support, transparent fees, tax reporting tools and compliance with FIC and Travel Rule requirements. A platform that ticks these boxes offers a stronger foundation than one chosen purely on trading volume or brand recognition.

- How much is 1 crypto in South Africa?

- "1 crypto" is not a standard unit. Prices depend entirely on the specific asset, whether Bitcoin, Ether, a stablecoin or another token. South Africans typically view prices converted to rand, and those values shift constantly in line with global market movements, so always check a live exchange rate.

Sources

Author

Crypto analyst and blockchain educator with over 8 years of experience in the digital asset space. Former fintech consultant at a major Wall Street firm turned full-time crypto journalist. Specializes in DeFi, tokenomics, and blockchain technology. His writing breaks down complex cryptocurrency concepts into actionable insights for both beginners and seasoned investors.