Blockchain Surveillance: How Crypto Tracking Works in 2026

What Is Blockchain Surveillance?

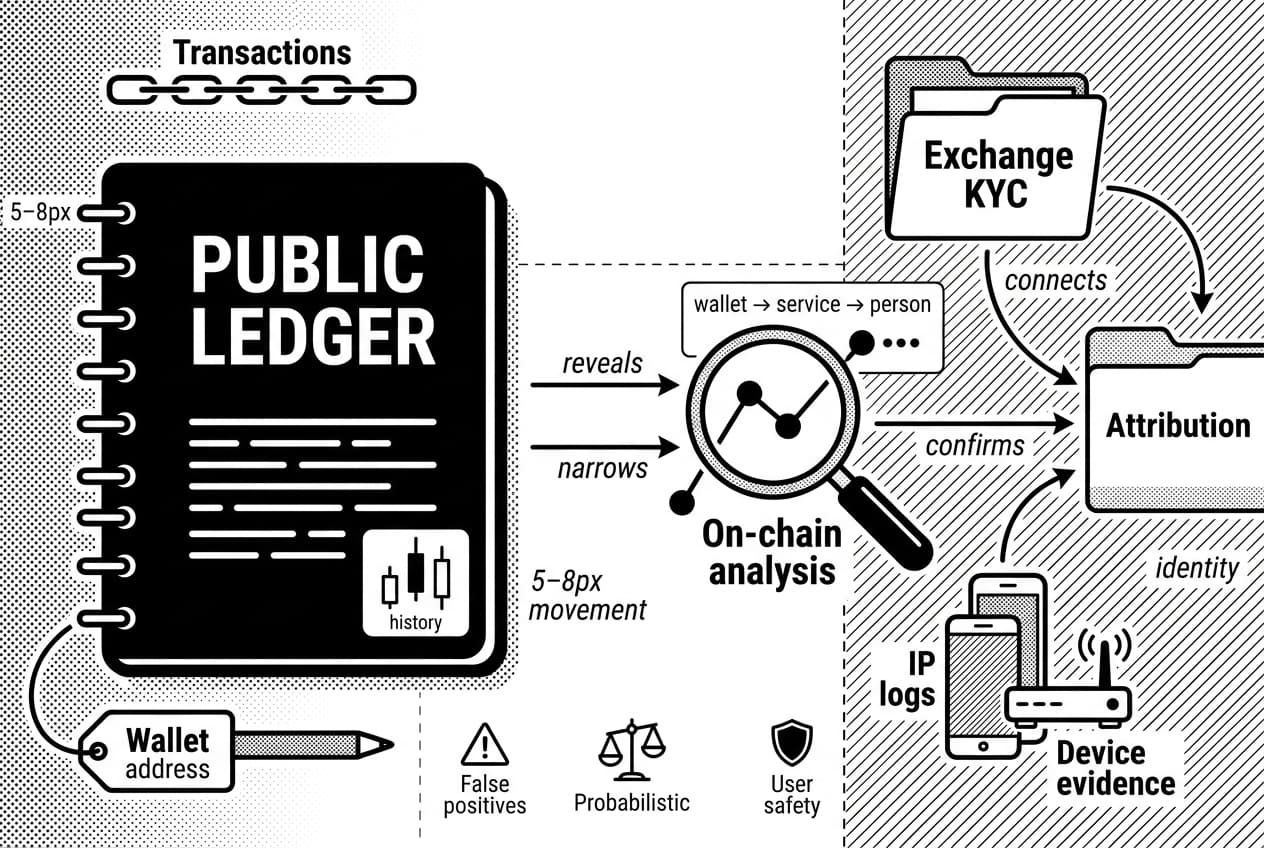

Blockchain surveillance is the practice of analyzing public blockchain records to follow crypto transactions, connect wallet activity to services or people, and support crypto tracking for compliance, fraud response and investigations.

Why It Matters

This affects ordinary users in 2026, not just hackers or exchanges. A deposit can be delayed because an exchange screening tool dislikes a wallet's history. A tax authority may request transaction records from a platform. A theft victim may need a trace report before police or an insurer can act. The key point is simple: public blockchains reveal movement, while identity usually comes from records outside the chain.

The common claim is that blockchain surveillance makes crypto fully traceable and therefore safe. A more accurate view is that surveillance is powerful but probabilistic. On-chain analysis narrows the search area. Strong attribution usually comes later, from exchange identity checks, IP logs, device evidence, subpoenas or admissions.

A Simple Analogy: A Shared Notebook Nobody Can Edit

A public blockchain works like a shared notebook that everyone can read and nobody can secretly rewrite after saving. Every transaction is a line in that notebook. A wallet address is like a public pen name: you can see what the pen name did, but the notebook does not automatically reveal the person holding the pen.

Andreas Antonopoulos, an independent author and Bitcoin educator, has long explained that Bitcoin is pseudonymous rather than anonymous. That difference matters because a pseudonym can collect a history. Once one address is linked to a real-world account, older and newer activity may become easier to connect.

Brief Background: From Block Explorers to Analytics Platforms

Bitcoin's first block was mined on Jan. 3, 2009 (Bitcoin developer reference, Jan. 2009). From the beginning, anyone could inspect the ledger, but early users mostly did that with basic block explorers, which are websites that display transaction IDs, addresses, amounts and timestamps in a readable format.

Analytics became more structured as exchanges, stablecoin issuers and law enforcement needed a way to screen deposits and trace stolen funds. Chainalysis estimated that illicit addresses received $24.2 billion in crypto value in 2023 (Chainalysis, Jan. 2024). That figure shows why the industry moved from manual lookup to large transaction graphs, wallet labels and automated risk scoring.

The Ledger-to-Identity Ladder

This article uses a simple framework called the ledger-to-identity ladder. It separates what the blockchain can show from what a real investigation still has to prove:

- Ledger fact: a transaction happened at a specific time, for a specific amount, between specific addresses.

- Service link: one address interacted with a known exchange, bridge, protocol, scam wallet or sanctioned address.

- Behavior pattern: multiple addresses behave as if they may be controlled together.

- Risk inference: the wallet is scored based on direct or indirect exposure to risky activity.

- Identity evidence: off-chain records connect a wallet to a person, company or device.

- Legal conclusion: investigators test whether the evidence proves control, knowledge and intent.

The higher you climb, the less the blockchain alone can do. Good blockchain surveillance respects that limit.

Why Public Blockchains Can Be Traced

Public blockchains can be traced because their transaction records are open by design. Bitcoin, Ethereum and many other networks publish address activity, amounts, timestamps and transaction hashes for anyone to inspect.

What a Transaction Reveals

If Alice sends 0.5 BTC to Bob, the Bitcoin network records the sending address, the receiving address, the amount, the fee and a transaction hash. A wallet address is a string of letters and numbers that receives or sends funds. A transaction hash is a unique receipt code for one transfer. A fee is the payment made to miners or validators for processing the transaction.

You can verify public transaction data with a block explorer, a free website that turns raw blockchain data into a readable search result. How to use a block explorer is simpler than many beginners expect. Legal names do not appear by default. Addresses do.

Pseudonymous Does Not Mean Anonymous

Anonymous means there is no identifying label. Pseudonymous means a substitute label is used instead of a real name. Most public crypto networks are pseudonymous. The address hides your name, but the address itself keeps a visible history of deposits, withdrawals, swaps and payments.

That history becomes more revealing when it touches a regulated exchange, a payment processor, a public profile or a social post. Understanding blockchain pseudonymity and anonymity is the starting point for understanding why crypto tracking works. The ledger does not need your name. It only needs one point where an address and identity meet.

Vitalik Buterin, co-founder of the Ethereum project, has repeatedly written about the tension between public verification and user privacy. That tension is visible here: blockchains need transparency so users can verify state, but that same transparency lets analysts build financial profiles from repeated activity.

How Blockchain Surveillance Companies Track Crypto Transactions

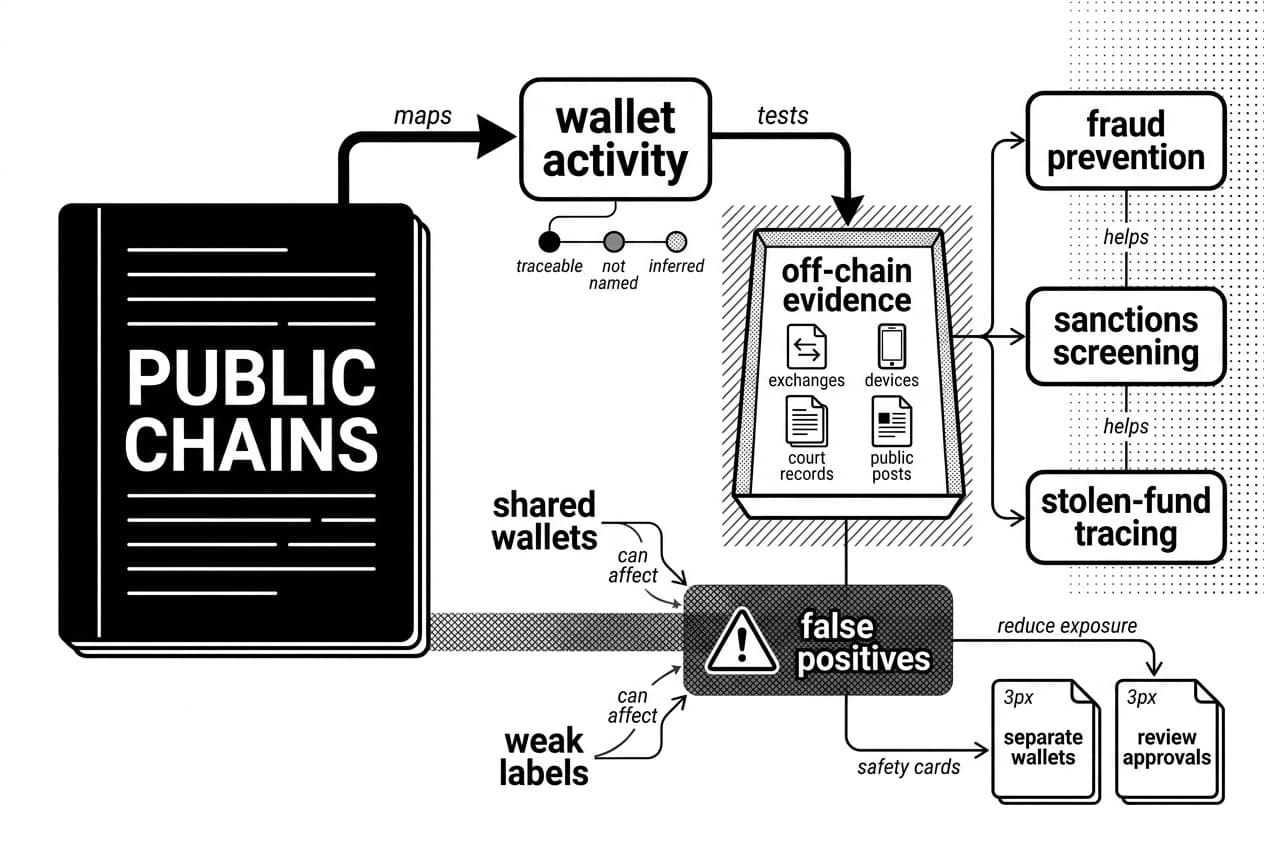

Blockchain surveillance companies turn public records into investigative leads through a step-by-step mapping process. The process is not magic. It starts with ledger data, adds labels, groups related activity, follows money movement and then checks the result against off-chain evidence.

- Collect on-chain data from public blockchains by running nodes and indexing transactions.

- Label known wallets tied to exchanges, protocols, scams, bridges, mixers and sanctioned entities.

- Cluster related addresses that appear likely to be controlled by the same user or organization.

- Trace fund flows across wallets, token swaps, bridges and services.

- Assign risk scores based on direct and indirect exposure to risky activity.

- Verify with off-chain evidence such as exchange records, court orders, device data and open-source research.

Step 1: Collect On-Chain Data

Analytics firms often run nodes, which are software clients that download and verify blockchain data. Running a node helps a firm avoid relying on a third-party feed. The firm then indexes blocks, addresses, token transfers and smart contract calls so they can be searched quickly.

The amount of data is large and growing. Layer 2 networks, which are systems that process transactions separately from a base chain and later settle data back to it, add another layer of tracking work. L2BEAT listed more than 100 Ethereum layer 2 and related scaling projects on its public dashboard (L2BEAT, July 2026).

Step 2: Label Known Wallets and Services

Raw addresses are just strings. Labels make them meaningful. A label may say that an address belongs to an exchange hot wallet, a DeFi lending pool, a bridge contract, a phishing wallet or a sanctioned service. Labels can come from public disclosures, exchange cooperation, blockchain explorers, sanctions notices, litigation records and direct investigations.

Labels differ in quality. A confirmed exchange address is much stronger evidence than a guess based on timing. Good crypto tracking systems should store the source, date and confidence level behind every label. Without that audit trail, a label can become a rumor inside a database.

Step 3: Cluster Wallets That Likely Belong Together

Wallet clustering means grouping addresses that appear to be controlled by the same person or organization. One common Bitcoin method is the common-input heuristic. If two addresses are used together as inputs in one transaction, the same wallet software may have signed for both. That can be a strong clue, but it is not perfect.

Other signals include repeated deposit behavior, similar fee choices, linked withdrawal patterns and timing. Willy Woo, an independent on-chain analyst, is known for using on-chain patterns to study market behavior. Surveillance firms apply a different goal to the same broad idea: they look for address behavior that may reveal control relationships.

Step 4: Trace Fund Flows

After labeling and clustering, analysts follow funds through transaction hops. A hop is one move from one address or contract to another. In simple theft cases, stolen funds may move from the victim address to a scam wallet and then to an exchange deposit address. In harder cases, funds may pass through token swaps, bridges and shared liquidity pools.

Tracing gets harder when value changes form. For example, ether may be swapped into a stablecoin, bridged to another chain and later sent to an exchange. The economic value may be the same, but the technical trail crosses contracts and networks.

Step 5: Score Risk and Build an Investigation Graph

A risk score is a software-generated estimate that a wallet or transaction is exposed to suspicious activity. Analysts often display this as a graph, where wallets and services are nodes and transfers are links. A wallet's score may rise after direct contact with a scam address, a sanctioned address or funds from a known hack.

The risky part is indirect exposure. A wallet may receive funds that passed through a suspicious address several hops earlier. That does not prove the wallet owner did anything wrong. It may only show proximity. This is where false positives can affect ordinary users, especially when shared exchange wallets or large liquidity pools are involved.

Step 6: Verify With Off-Chain Evidence

The final step is verification. Strong teams treat blockchain analytics as a lead, not a verdict. They compare the graph with exchange identity records, IP logs, legal filings, open-source posts, device evidence or victim reports. Without that second layer, a trace may show movement but not control, knowledge or intent.

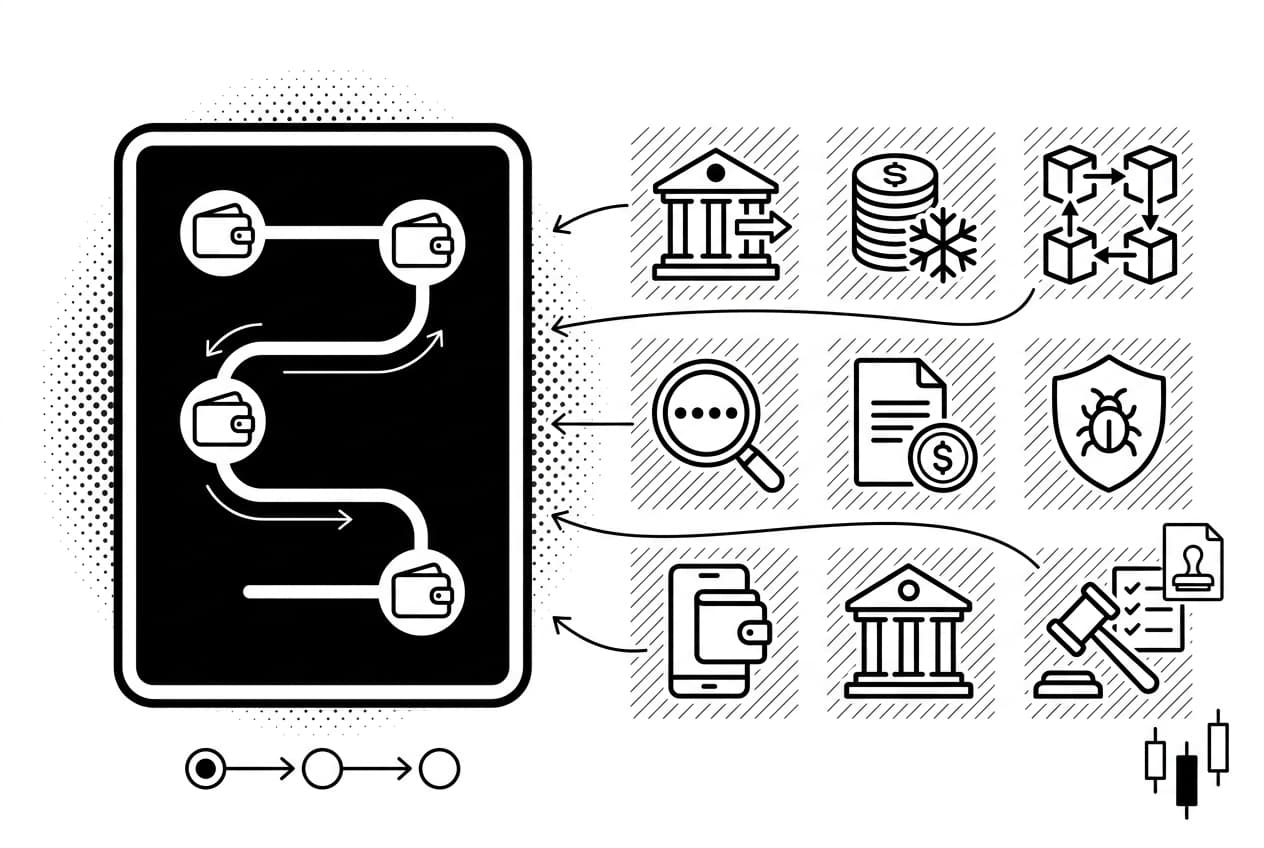

What Data Sources Make Crypto Tracking More Powerful?

Crypto tracking becomes more powerful when public ledger data is combined with off-chain records. On-chain data shows what happened between addresses. Off-chain data can help show who controlled an account, where a login came from or why a transfer occurred.

On-Chain vs. Off-Chain Data

On-chain data is information written directly to a blockchain, such as wallet addresses, transaction amounts, timestamps and smart contract calls. Off-chain data is information stored outside the blockchain, such as exchange identity checks, support tickets, IP logs, social posts and court records.

Data type | Examples | What it helps prove | Limitations |

|---|---|---|---|

On-chain data | Transaction hashes, wallet balances, smart contract calls, block timestamps | Fund movement, transaction timing, wallet interaction and possible clustering | Addresses are pseudonymous; legal names are not attached by default |

Off-chain data | KYC records, IP logs, subpoenas, social posts, support tickets, device evidence | Identity, account access, location clues and possible intent | May require legal process, may be incomplete, and can still be misread |

KYC means know your customer, the identity check many regulated exchanges perform before allowing full account access. If a wallet deposits funds to a KYC exchange, the exchange may be able to link that deposit to a verified account. A government agency may then request those records through legal process.

An Evidence Matrix for 2026

The table below is a practical evidence matrix for reading surveillance claims. It is not a legal standard. It is a way to separate weak signals from stronger proof.

Evidence type | Typical strength | Why it matters |

|---|---|---|

Single wallet interaction | Low to medium | Shows contact, but not identity or intent. |

Repeated pattern across addresses | Medium | May support clustering, but heuristics can fail. |

Confirmed exchange deposit | Medium to high | May connect an address to an account record. |

Exchange KYC response | High | Can link an account to a verified person, subject to accuracy. |

Device or IP evidence | High | Can support control or access, but still needs context. |

Direct admission or signed message | Very high | Can strongly support control when properly authenticated. |

Public case records show why this distinction matters. The U.S. justice department said investigators recovered 63.7 bitcoin from a ransomware payment in June 2021 (DOJ, June 2021). The public announcement described blockchain tracing, but recovery also depended on control of a private key. The ledger helped map the funds. Access evidence helped recover them.

How AI Helps, and Where It Can Mislead

AI models can scan large transaction graphs faster than a human team. They can flag sudden volume spikes, funds split across many wallets, repeated bridge patterns or behavior similar to known laundering routes. That speed is useful when stolen funds move within minutes.

The danger is overconfidence. A model may flag a wallet because it shared an exchange deposit route with risky funds, interacted with a common contract or received dust. A flagged wallet is not a convicted wallet. Human review and off-chain checks are still needed before a serious decision, such as an account freeze or legal report.

Who Uses Blockchain Surveillance and Why?

Blockchain surveillance is used by exchanges, stablecoin issuers, DeFi teams, investigators, tax agencies, cybersecurity firms and individual users. Each group has a different goal, but the basic method is the same: follow public wallet activity and add context where possible.

Fraud, Hacks and Market Abuse

After a hack, stolen funds rarely sit still. They may move through swaps, bridges, new wallets and exchanges. Investigators trace those hops to find a cash-out point or a service that can freeze funds. Chainalysis reported that stolen crypto funds fell to about $1.7 billion in 2023 (Chainalysis, Jan. 2024). Even at that lower level, real-time tracking matters because attackers often move quickly.

The same tools can help investigate phishing, ransomware, fake token launches and market manipulation. In each case, the chain can show where funds moved. It cannot, by itself, prove who planned the scheme.

Compliance for Exchanges and Institutions

Regulated exchanges screen deposits and withdrawals for sanctions, fraud and money-laundering risk. They do this because banks, regulators and licensing rules require them to understand customer activity and source of funds. Institutions also need organized records for crypto tax reporting help, especially when DeFi trades, airdrops or NFT sales create taxable events.

The FATF said in a June 2023 update that implementation of its virtual asset standards remained uneven across jurisdictions (FATF, June 2023). That uneven rollout is one reason crypto tracking rules can feel inconsistent from one exchange or country to another.

Everyday User Safety

You do not need an enterprise analytics account to protect yourself. Free block explorers can show token approvals, unexpected transfers and unfamiliar contracts. A practical first step is to paste your own address into a block explorer and review recent activity. If you see a transaction you did not approve, check if your wallet is compromised before sending more funds.

- Law enforcement and tax agencies combine court-ordered records with on-chain tracing.

- Stablecoin issuers may freeze tokens at the contract level when legally required.

- DeFi risk teams screen wallets that interact with protocol front ends.

- Cybersecurity firms track ransomware wallets and attacker infrastructure.

- Individual users can review transfers and approvals with public tools.

What Blockchain Surveillance Can and Cannot Prove

Blockchain analytics can prove that a transaction happened. It can often show that funds touched a wallet, exchange or contract. It cannot prove legal identity, intent or guilt by itself.

Can often show | Cannot prove by itself |

|---|---|

Where funds moved between addresses | The legal identity of the wallet owner |

Which exchange or service received funds | Who authorized or initiated the transaction |

That two wallets interacted with each other | Whether the recipient knew the origin of funds |

Transaction timing and amount | The purpose or intent behind a transfer |

A cluster of addresses behaving similarly | That one person controlled every clustered address |

Common Sources of Error

False positives can happen when shared services mix many users together. Large exchange wallets may pool deposits from thousands or millions of customers. If a screening tool treats the shared wallet as suspicious without deeper review, innocent users can be swept into the same risk bucket.

Other errors come from hostile tactics. Dusting means sending tiny amounts of crypto to a wallet to create a trackable connection or spam the address history. Address poisoning means sending a transaction from a lookalike address so the victim later copies the wrong address. Both tactics can pollute transaction history.

Smart contracts add more complexity. A smart contract is code on a blockchain that can hold and move assets according to preset rules. When a user interacts with a DeFi protocol, funds may pass through several contracts before reaching the final destination. Mislabeling one contract can affect many unrelated users.

Why Attribution Usually Needs More Than a Wallet Address

The strongest investigations combine on-chain tracing with off-chain proof. A wallet address alone is not a passport, fingerprint or confession. It is a public identifier that may or may not be controlled by the person an investigator suspects.

Andreas Antonopoulos has emphasized that pseudonymity is real, even though it is fragile. That is the right balance for readers to remember. Blockchain surveillance can reveal patterns that would be impossible in cash. Still, a court-ready case usually needs exchange records, device evidence, account access logs or other corroboration.

In 2026, the safest way to read a surveillance report is to ask two questions: what does the chain prove directly, and what outside evidence supports the identity claim? If those two questions are kept separate, the analysis is much less likely to overstate what the ledger can show.

Privacy Tools, Mixers, Bridges and Privacy Coins

Privacy tools exist because public ledgers expose more financial detail than many users expect. Some tools are used for legitimate confidentiality. Some are used to hide crime. The same technical feature can raise very different legal and ethical questions depending on context.

Why Some Tools Break Simple Transaction Trails

Mixers and CoinJoin-style transactions combine funds from multiple users and return equivalent amounts to new addresses. The goal is to make it harder to link a specific input with a specific output. They do not erase the fact that funds entered or left the tool.

Bridges move value between blockchains. Because each chain has its own ledger, a simple search on one chain may not show the full path across another. Privacy coins use cryptography to hide some transaction details by default. Zero-knowledge privacy technology uses a different method: it lets someone prove a statement is true without revealing the underlying data.

Privacy tools are not invisibility cloaks. Reusing an address, posting a wallet publicly or cashing out through a KYC exchange can undo a careful privacy setup. The U.S. treasury sanctioned a major Ethereum mixer on Aug. 8, 2022 (U.S. treasury, Aug. 2022). That action showed that regulators may target infrastructure, not only individual users.

The Legal and Ethical Line

Financial privacy can be legitimate. A business may want to hide supplier payments from competitors. A journalist may need donor privacy. A user may simply dislike exposing a full spending history to strangers. Those reasons differ from hiding ransomware payments, fraud proceeds or stolen assets.

The practical risk is that compliance systems may not know your intent. If your wallet touches a sanctioned or high-risk service, exchanges may freeze funds or ask for explanations. Some jurisdictions also pressure exchanges to limit support for privacy-focused assets. Before using any privacy tool, check local law and understand that a wallet's history can follow it for years.

- Mixers and CoinJoin-style transactions can break direct links, but they do not remove every trace.

- Bridges and cross-chain swaps create gaps in simple tracing, not complete blind spots.

- Privacy coins and zero-knowledge proofs hide more data at the protocol or proof level.

- Human mistakes, such as address reuse, often defeat technical privacy.

- Legal risk is real when a wallet touches sanctioned or high-risk services.

What Blockchain Surveillance Means for Your Privacy in 2026

Every public on-chain action can become part of a permanent profile. Connecting an ENS name to a wallet, posting a donation address, buying an NFT and then depositing to an exchange can give analysts enough clues to connect public activity with a real person.

By 2026, crypto tracking is stronger because exchanges hold more identity data, analytics tools cover more chains and AI systems can scan larger graphs. The privacy lesson is not panic. It is separation. Do not mix public identity, savings, trading, donations and experimental DeFi activity in one address if you can avoid it.

Simple Habits That Reduce Unnecessary Exposure

Good privacy hygiene is mostly a set of small, repeatable habits:

- Do not post wallet addresses publicly. A public address can reveal years of activity.

- Separate wallets by purpose. Keep public activity, savings and experiments apart.

- Understand exchange deposits. A KYC exchange can connect a deposit address to your verified account. Learn more about self-custody and exchange wallet risks before choosing where to hold funds.

- Review token approvals. Old approvals can let a contract move tokens later. You can revoke risky token approvals in a few minutes.

- Read your own address history. Check what a stranger would see in a block explorer.

Vitalik Buterin has argued that privacy should be treated as a normal part of blockchain design, not only as a tool for suspicious users. That framing is useful for everyday users: privacy hygiene is not an admission of wrongdoing. It is basic financial self-protection.

When to Get Professional Help

Some situations go beyond personal habits. If funds were stolen, an exchange froze your account, a wallet was flagged, or you received a legal notice, slow down and document everything. Save transaction hashes, screenshots, support tickets and dates before changing wallet setups.

Contact the exchange first if your account is frozen. For stolen funds, a blockchain security firm may be able to prepare a trace report for law enforcement. For taxes, use a qualified accountant who understands crypto transactions. If legal exposure is possible, read our guide on when to hire a crypto lawyer before making official statements.

Key Takeaways

Blockchain Surveillance in One Minute

Blockchain surveillance maps public wallet activity, then tests that map against off-chain evidence. It is useful for fraud prevention, sanctions screening and stolen-fund tracing. It is also imperfect, because wallet ownership and intent are inferred from evidence rather than written directly into the ledger.

- Public chains are traceable, but wallet owners are not named by default.

- Identity usually comes from exchanges, devices, court records or public posts.

- Crypto tracking helps fight fraud, hacks, ransomware and sanctions evasion.

- False positives can affect innocent users through shared wallets or weak labels.

- Separate wallets and review approvals to reduce avoidable exposure.

Frequently Asked Questions

- Can the blockchain be traced?

- Most public blockchains can be traced because every transaction, address, amount and timestamp is openly recorded. That said, tracing a transaction is much easier than proving who owns a wallet. Connecting an address to a real person typically requires off-chain evidence such as exchange records, IP logs or legal documents.

- Is it possible to track crypto?

- Yes, for many cryptocurrencies. Bitcoin and Ethereum use public ledgers that blockchain surveillance companies analyze using wallet labeling, clustering algorithms and transaction graphs. Tracking does have limits though — privacy tools, cross-chain bridges, shared exchange wallets and false positives can all complicate or undermine the analysis.

- Can the FBI trace a Bitcoin wallet?

- Yes. Law enforcement agencies use public blockchain data, commercial analytics platforms and legal subpoenas to exchanges or service providers to trace Bitcoin wallet activity. However, a wallet address alone rarely identifies a person — investigators typically need supporting off-chain evidence to build a conclusive case.

- Which crypto can be tracked?

- Cryptocurrencies with public ledgers — including Bitcoin, Ethereum, Solana and most ERC-20 tokens — can generally be tracked at the transaction level. Privacy-focused coins and certain mixing protocols are harder to analyze, but cash-out points and off-chain records such as exchange KYC data can still expose identities.

- What is the best crypto tracker?

- There is no single best tool — it depends on what you need. Block explorers work well for quick public lookups, portfolio trackers manage personal balances, tax software handles reporting, and enterprise blockchain surveillance platforms are built for compliance teams and criminal investigators. Match the tool to your specific purpose.

- Is blockchain security real?

- Yes, in the sense that cryptography and consensus mechanisms make it extremely difficult to alter a recorded transaction. However, users still face serious risks from phishing attacks, stolen private keys, malicious smart contracts, exchange failures and poor personal wallet practices — most losses come from human error, not the ledger itself.

- What is an example of blockchain security?

- Bitcoin's proof-of-work consensus and cryptographic signatures are straightforward examples. A cryptographic signature is a mathematical proof that the wallet's private key authorized a specific transaction — without ever exposing the private key itself. This mechanism prevents anyone from forging or altering transactions on your behalf.

Sources

Author

Crypto analyst and blockchain educator with over 8 years of experience in the digital asset space. Former fintech consultant at a major Wall Street firm turned full-time crypto journalist. Specializes in DeFi, tokenomics, and blockchain technology. His writing breaks down complex cryptocurrency concepts into actionable insights for both beginners and seasoned investors.