Crypto Regulation Latin America: Mexico, Argentina, Colombia

Crypto Regulation Latin America: Mexico, Argentina and Colombia

What Crypto Regulation in Latin America Means in 2026

Crypto regulation in Latin America means the laws, taxes, anti-money laundering rules and regulator supervision that govern how people and companies buy, sell, hold, transfer and cash out digital assets through exchanges, banks, wallets and payment providers.

Why It Matters

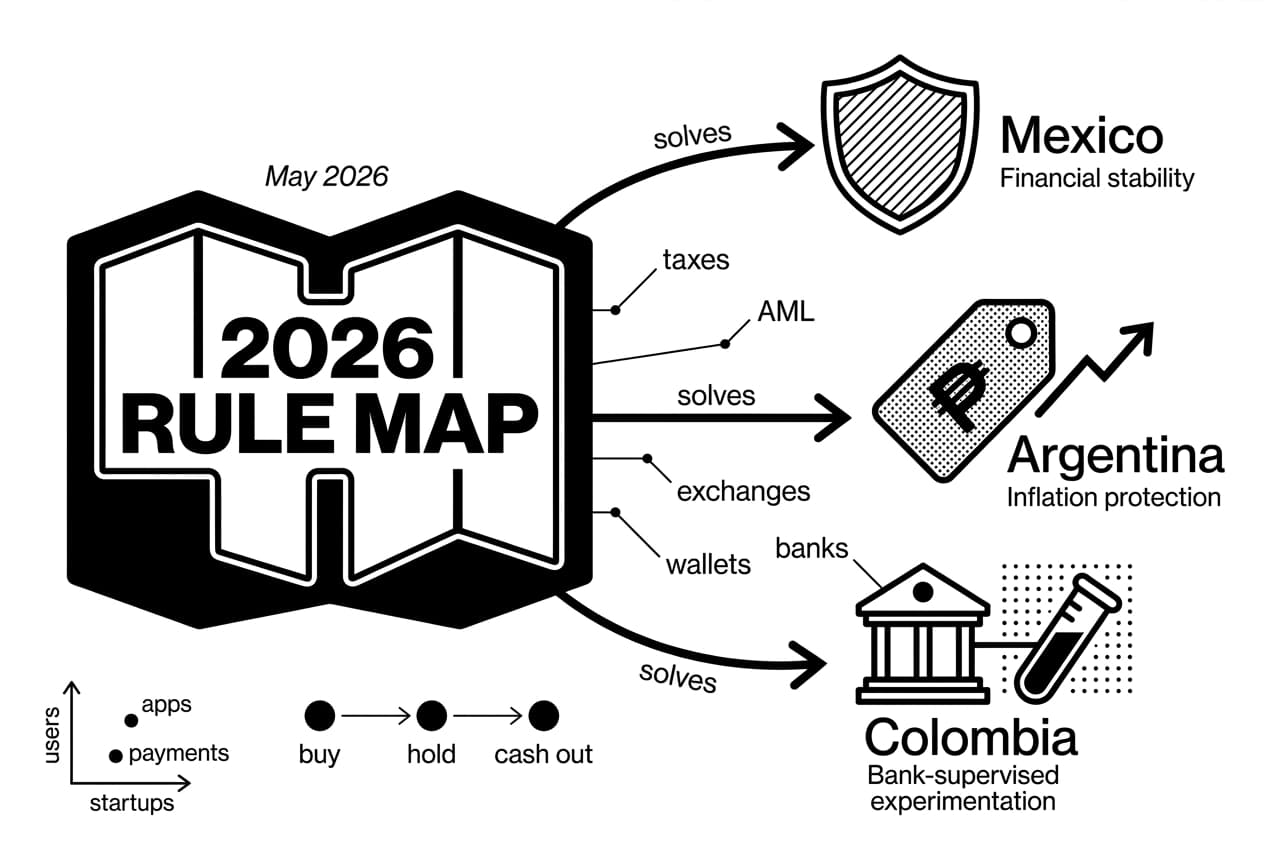

As of May 2026, a person buying bitcoin on a phone app faces a different rule set from a startup offering crypto payments or a compliance team approving exchange accounts. Mexico, Argentina and Colombia do not regulate one shared regional market. They regulate three different problems: financial stability, inflation protection and bank-supervised experimentation.

This article uses our Three-Problem Regulatory Map, an original country-by-country framework built from official regulator publications, tax guidance and public market data. The map asks one practical question for each country: what problem is the regulator trying to solve first? That lens prevents the common mistake of treating crypto regulation latin america as one uniform compliance playbook.

A Simple Definition for Beginners

A cryptocurrency is digital money secured by cryptography, meaning code that protects transactions from tampering. Bitcoin and ether are the best-known examples. A digital asset is broader and can include cryptocurrencies, tokenized securities and non-fungible tokens. An exchange is a marketplace where users buy and sell crypto. A wallet stores the private keys that control access to crypto. For a fuller wallet explanation, see our guide to custodial vs non-custodial crypto wallets.

Anti-money laundering, or AML, means rules that require financial businesses to identify customers and report suspicious transactions. Know your customer, or KYC, is the identity-checking step inside AML. Legal tender means money that creditors must accept for debts. Crypto is generally legal to own in Mexico, Argentina and Colombia, but it is not legal tender in those three countries.

Think of a blockchain like a shared Google Doc that nobody can edit after saving: everyone can verify the record, but a regulator still decides which companies may provide the on-ramps, off-ramps and customer-facing services.

Background: Why the Region Became a Crypto Hotspot

Crypto use grew for practical reasons. Mexico received about $63.3 billion in remittances during 2023, a figure reported by Banco de México, 2024. That money-flow reality makes cheaper cross-border payment rails attractive, even when banks and regulators remain cautious.

Argentina had a different trigger. Consumer prices rose 211.4% year over year in December 2023, according to INDEC, January 2024. For many households, dollar-linked stablecoins became a way to preserve purchasing power when local-currency savings lost value quickly.

Colombia followed a third path. Its financial regulator backed supervised tests between banks and crypto firms rather than jumping straight to a full national license. The 2020 sandbox period was documented in public central-bank and supervisory discussions, including BIS working paper material, 2020.

Lyn Alden, founder of Lyn Alden Investment Strategy, has often framed dollar scarcity and weak local currencies as key reasons people seek dollar-denominated assets. That macro explanation fits Argentina best, but it does not fully explain Mexico or Colombia. That is why the country-by-country approach matters.

Why Latin America Regulates Crypto Differently by Country

The regional pattern is not prohibition. It is selective control. Individuals can usually hold crypto, while exchanges, payment companies and financial institutions face registration, reporting and tax obligations. The details change sharply by jurisdiction.

The Three-Problem Regulatory Map

Country | Primary regulatory problem | What that means in practice |

|---|---|---|

Mexico | Financial stability | Keep regulated banks and fintech firms from offering crypto without central-bank approval. |

Argentina | Inflation and informal dollar access | Bring high crypto use into registration, tax and consumer-protection systems. |

Colombia | Bank-supervised experimentation | Test bank and crypto partnerships under regulator observation before writing permanent rules. |

This framework is the article’s main information-gain layer: it turns scattered official rules into a practical decision model for users, investors, startups and compliance teams.

The Main Regulatory Tools: AML, Tax, Banking and Licensing

Most crypto rules use four tools. First, AML and counter-terrorist financing rules force exchanges to verify customers and watch for suspicious flows. Second, tax rules require users to report profits, income or assets. Third, banking rules decide whether crypto companies can access accounts and payment rails. Fourth, licensing or registration rules decide which companies may legally serve local users.

The financial action task force, October 2021 guidance on virtual assets pushed member countries to strengthen AML controls for exchanges and other virtual asset service providers. Its travel rule asks firms to pass sender and receiver information with covered transfers, which pulls crypto compliance closer to traditional wire-transfer compliance.

Central banks are also studying public digital money. You can track central bank digital currency projects to see how official digital-money work sits beside private crypto regulation.

- AML and KYC require exchanges to identify customers and report suspicious transactions.

- Tax reporting means crypto profits may be taxable even when crypto is not legal tender.

- Banking limits can block exchanges from easy fiat deposits and withdrawals.

- Licensing or registration separates permitted providers from informal platforms.

- FATF pressure is the strongest shared driver across the region.

Mexico Crypto Regulation: What Users and Businesses Need to Know

Yes, crypto is regulated in Mexico. Mexico crypto regulation separates individual ownership from regulated financial services: people can generally buy and hold digital assets, while banks, fintech firms and exchanges face strict authorization, AML and reporting duties.

Is Crypto Regulated in Mexico?

Mexico’s core framework is its fintech law, published on March 9, 2018 in the official federal gazette, March 2018. The law classifies crypto as virtual assets, not legal tender. That means bitcoin is property-like for regulatory purposes, but a shop is not required to accept it instead of pesos.

The central bank controls whether regulated financial institutions may use virtual assets internally or offer them to customers. The banking and securities supervisor oversees fintech institutions and AML controls. As of May 2026, this approval-heavy design is why mainstream Mexican banks remain cautious about direct crypto products.

Mexico’s AML and FATF Pressure

For businesses, AML is the strictest part of the rulebook. A Mexican exchange or crypto payment provider must identify customers, keep records, watch for suspicious activity and report red flags to the financial-intelligence authority. Personal use is different. Holding bitcoin in a private wallet is not the same as operating a platform that processes customer trades.

Hester Peirce, commissioner at the U.S. Securities and Exchange Commission, has repeatedly warned in public policy statements that unclear crypto rules can push activity outside supervised channels. That point is useful for Mexico: heavy approval rules may reduce bank exposure, but they can also push some users toward offshore or peer-to-peer platforms.

Taxes and Everyday Investing in Mexico

Mexico’s tax authority expects taxpayers to disclose taxable gains where crypto sales produce income. A simple example: if a person buys bitcoin for 500,000 pesos and later sells for 700,000 pesos, the 200,000-peso difference is the gain that needs tax analysis. The tax authority’s public portal continued to address digital tax compliance in SAT materials, 2022.

The exact tax treatment can depend on whether the person is an individual, a business, a frequent trader or a professional service provider. Cost basis, exchange-rate conversion and records matter. A qualified Mexican tax adviser is the safest source for filing decisions.

- Individuals can generally own crypto, but crypto is not legal tender.

- The 2018 fintech law created the virtual-asset category and fintech oversight path.

- Businesses face AML duties, including customer checks and suspicious-activity reporting.

- Taxable gains require records, including purchase price, sale price and dates.

- Bank access is limited because approval for regulated crypto services remains hard to obtain.

Argentina Crypto Regulation: Adoption, Inflation and New Oversight

Argentina’s crypto rules developed in response to heavy retail use. The country’s inflation problem made stablecoins popular before regulators had a mature licensing framework, so policy now focuses on registration, tax reporting and consumer protection.

Why Stablecoins Matter in Argentina

A stablecoin is a crypto token designed to track another asset, usually the U.S. dollar. USDT and USDC are common examples. They can reduce exposure to local-currency depreciation, but they add issuer risk, custody risk and platform risk. The token is only as reliable as the issuer, reserves and exchange access behind it.

Argentina’s 211.4% annual inflation figure for December 2023, reported by INDEC, January 2024, explains why many users care more about dollar access than speculative trading. Lyn Alden, founder of Lyn Alden Investment Strategy, has written extensively about why people in weak-currency economies seek harder or dollar-linked assets, while still warning that custodians and issuers introduce counterparty risk.

Exchange Registration and Consumer Protection

Argentina moved toward formal supervision through a virtual asset service provider registry. Law 27,739, tied to AML reforms, was published in Argentina’s official bulletin, March 2024, and the securities regulator later required crypto service providers to register before serving users locally.

Registration does not make a platform risk-free. It does create a paper trail. Users get a clearer route for complaints, and authorities can identify the companies serving the market. Unregistered offshore platforms may still be accessible online, but their legal and recovery risks are higher.

Argentina Tax Considerations

Crypto taxation in Argentina can involve income tax, capital gains analysis, asset reporting and the national wealth tax. The result depends on residence, asset location, trading frequency and whether the crypto was sold, earned, mined, staked or simply held at year-end.

For ordinary users, the safest rule is to keep dated records: acquisition price, sale price, platform, wallet address and local-currency value. For companies, the issue is broader because crypto receipts, treasury holdings and customer balances may create accounting as well as tax obligations.

- Stablecoins are widely used as dollar-linked savings tools, but issuer and custody risks remain.

- VASP registration began in 2024 as Argentina moved from informal tolerance to formal oversight.

- Inflation drives adoption more than in Mexico or Colombia.

- Tax treatment is fact-specific and can touch income, gains and asset reporting.

- Users should prefer registered providers when local consumer-protection options matter.

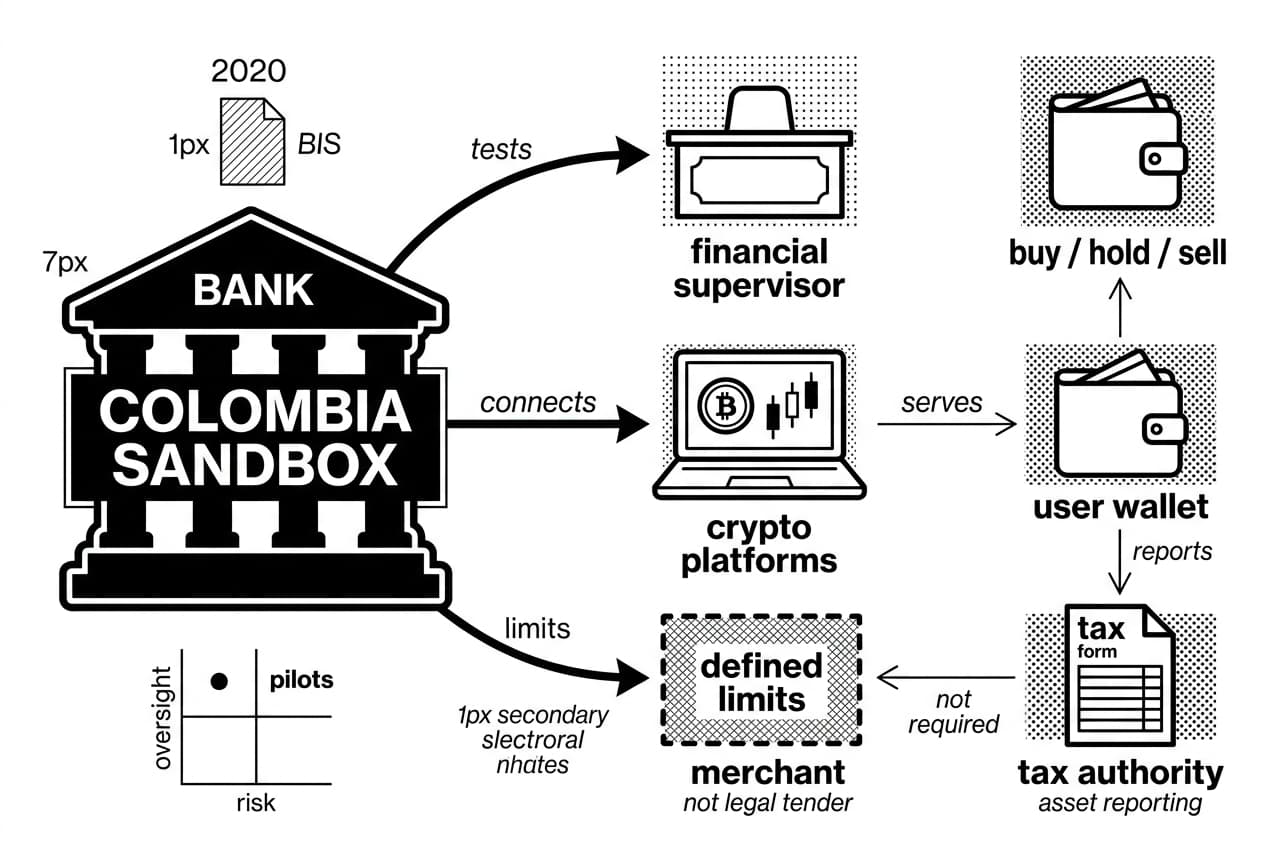

Colombia Crypto Regulation: Sandboxes, Banks and Tax Rules

Colombia’s approach is experimental and bank-centered. Instead of first writing a single nationwide crypto license, regulators allowed limited pilots so banks and crypto firms could test services under supervision.

How Colombia’s Regulatory Sandbox Worked

A regulatory sandbox is a supervised test space where companies try a financial product with regulator oversight and defined limits. Colombia’s financial supervisor supported crypto-bank pilots starting in 2020, with the model discussed in BIS working paper material, 2020. The goal was to learn whether banks could connect to crypto platforms without exposing the wider financial system to unmanaged risk.

The sandbox did not make crypto legal tender. It gave selected firms a legal testing route. That matters for startups because early regulator contact can reduce enforcement uncertainty. It also matters for users because a supervised pilot is safer than an informal product with no clear accountable party. You can compare this with other public digital-money tests in our CBDC pilot tracker.

Can Colombians Buy and Hold Crypto?

Yes. Colombians can generally buy, hold and sell crypto. The country does not treat bitcoin as legal tender, and merchants are not required to accept it. The tougher rules apply to platforms that provide exchange, custody or payment services, especially when they handle fiat deposits and withdrawals.

Colombia Tax and Reporting Basics

Colombia’s tax authority has treated crypto as an asset for reporting and tax purposes. If a person buys ETH for $1,000 and later sells it for $1,500, the $500 gain is the number that tax analysis starts with. Public tax guidance remained active in DIAN materials, 2023.

Colombia is clearer than Argentina on treating crypto as a reportable asset, but less settled than Mexico on a full business licensing route. Compliance teams should watch tax authority notices, financial-supervisor statements and any new legislative bills before launching a product.

- Sandbox first: Colombia tested bank and crypto connections before permanent licensing.

- Individual access is open: users can generally buy and hold crypto.

- Crypto is an asset, not currency: it can be taxable and reportable.

- Platform rules are stricter: businesses face AML, banking and reporting duties.

- Rules are still developing: legal certainty depends on the product type.

Mexico vs Argentina vs Colombia: Side-by-Side Comparison

Crypto regulation in Latin America is not a single rulebook. Mexico is approval-heavy, Argentina is adoption-heavy and Colombia is sandbox-heavy. The comparison below is designed for quick extraction by users, investors, startups and compliance teams.

Country | Legal status | Main regulator focus | Exchange obligations | Tax notes | Key user risk |

|---|---|---|---|---|---|

Mexico | Legal to own; not legal tender | Financial stability and fintech control | AML controls, fintech registration, central-bank approval for regulated use | Gains may be taxable income | Limited bank access and offshore-platform risk |

Argentina | Legal to own; not legal tender | VASP registration and inflation-driven usage | Registry, AML reporting and consumer-protection duties | Income, gains and wealth-tax issues can apply | Currency controls, unstable rules and custody risk |

Colombia | Legal to own; not legal tender | Supervised bank and crypto pilots | AML reporting, pilot approval and platform monitoring | Crypto treated as a reportable asset | No final all-purpose crypto license yet |

Brian Armstrong, co-founder and chief executive of Coinbase, has publicly argued that fragmented crypto rules increase the burden on exchanges trying to operate across borders. That observation fits this three-country comparison: one regional launch plan will miss local requirements.

What Is Similar Across the Three Countries?

- Crypto is not legal tender in Mexico, Argentina or Colombia.

- Individuals can generally buy and hold crypto, subject to tax and platform rules.

- Exchanges face stronger AML, KYC and reporting expectations.

- Tax authorities increasingly expect records of gains, income and asset balances.

- Banks remain cautious, especially when crypto firms need fiat accounts.

What Is Different?

Mexico has the clearest statutory starting point because the 2018 fintech law already defines virtual assets. Argentina has the strongest retail adoption pressure because inflation made dollar-linked tokens useful for households. Colombia has the most structured testing model because regulators used supervised pilots to learn from limited live products.

The practical takeaway is simple. If you are an ordinary saver worried about inflation, Argentina’s stablecoin access is the central issue. If you are a startup choosing a market, Mexico offers clearer rules but a higher approval bar. If you are a bank or fintech testing a product, Colombia rewards early regulator engagement.

Taxes, Banks and Cashing Out Crypto in Latin America

Cashing out means selling crypto for local currency and withdrawing that money to a bank account, payment app or cash channel. The trade itself may be simple, but the tax and banking questions can be difficult.

How Crypto Investors Typically Cash Out

- Choose a regulated or reputable platform. Look for local registration, clear fees and withdrawal support.

- Complete KYC. The platform verifies identity before allowing fiat withdrawals.

- Sell the asset. The user places a market order or limit order.

- Withdraw local currency. Funds move to a bank account or payment app.

- Keep records. Save trade confirmations, wallet addresses, bank receipts and tax calculations.

Bank friction is common. A bank may ask why funds arrived from an exchange, especially after a large withdrawal or repeated peer-to-peer transfers. Organized records are the user’s best defense. Businesses that want to reduce some bank friction can also study how to accept Bitcoin Lightning payments for business, though tax and AML duties still apply.

Lyn Alden, founder of Lyn Alden Investment Strategy, has noted that people in inflationary economies often delay conversion back into local currency. That choice may make economic sense, but it can change the timing of taxable events, depending on local law.

Do Small Crypto Gains Need to Be Reported?

There is no single regional threshold that makes small gains automatically tax-free. Mexico, Argentina and Colombia each apply domestic tax rules. A $3,000 gain may be treated differently depending on residency, whether the gain came from trading, staking or business income, and whether local law classifies the asset as property, income or a financial instrument.

Users should keep records even for small trades. A tiny gain today can become hard to reconstruct later if the platform closes, a wallet address changes or a tax authority asks for source-of-funds evidence.

- Cash-out steps matter: platform choice, KYC, sale, withdrawal and records.

- Bank freezes can happen: documentation helps explain source of funds.

- Small gains are not automatically exempt: local tax law controls.

- Residency matters: where you pay tax may differ from where the platform is based.

- Professional advice is prudent: a local accountant can interpret the facts.

Compliance Risks for Crypto Companies Operating in LATAM

A crypto company should not use one generic regional policy for Mexico, Argentina and Colombia. Each country needs its own licensing, AML, tax, sanctions and banking review.

Money Laundering, Sanctions and OTC Risk

AML means anti-money laundering: rules that require firms to detect, prevent and report suspicious financial activity. OTC, or over-the-counter trading, means large trades arranged directly between parties rather than through a public order book. OTC desks can carry higher risk because trade size, counterparties and source of funds require closer review.

Sanctions risk is especially important when transactions cross borders or touch privacy tools. The U.S. Treasury action against Tornado Cash in Reuters reporting, August 2022 still influences compliance teams. For more detail, see our analysis of the Tornado Cash court case and privacy-tool impact.

A Practical Compliance Checklist

AML means anti-money laundering, the set of controls that requires crypto businesses to identify customers, monitor transactions and report suspicious activity. Before launching in any LATAM market, teams should:

- Map local licenses before accepting users in Mexico, Argentina or Colombia.

- Verify customer identity with government ID, address checks and enhanced due diligence for higher-risk accounts.

- Monitor transactions for unusual size, velocity, wallet behavior and source-of-funds concerns.

- Screen sanctions lists before onboarding and before processing high-risk transfers.

- Record KYC evidence, transaction logs, wallet-risk scores and compliance decisions for audit review.

- Document tax treatment for fees, customer trades, treasury holdings and local reporting duties.

- Update policies whenever regulators publish new guidance, registration rules or enforcement notices.

Key Takeaways

The Bottom Line for Readers

- Mexico has the clearest legal starting point through its 2018 fintech law, but regulated crypto services remain approval-heavy.

- Argentina has intense user demand because of inflation, while its 2024 VASP registry pushes crypto firms toward formal oversight.

- Colombia has used supervised pilots to test bank and crypto products before finalizing a broad licensing model.

- Taxes cannot be ignored: gains, income and asset reporting may apply even when crypto is not legal tender.

- This article is educational only: verify current rules with a licensed local attorney, accountant or official regulator before making decisions.

Frequently Asked Questions

- Is crypto regulated in Mexico?

- Yes, though the rules vary by who you are. Individuals can generally buy and hold crypto, but financial institutions, fintechs and virtual asset service providers face strict AML, reporting and central bank requirements. Bitcoin is not legal tender in Mexico, and the regulatory landscape continues to evolve.

- Is BTC still legal tender in El Salvador?

- El Salvador made bitcoin legal tender in 2021, making it a regional outlier. This article focuses on Mexico, Argentina and Colombia, where bitcoin holds no legal tender status. El Salvador's approach is unique and should not be treated as a template for how Latin America broadly handles crypto regulation.

- Which countries have banned crypto?

- Very few countries have imposed outright bans. Most restrict how banks, payment systems or exchanges interact with crypto rather than banning ownership entirely. Mexico, Argentina and Colombia each regulate access and compliance differently, but none represent a full prohibition model for users holding or trading digital assets.

- Which bank is crypto friendly in Latin America?

- No single bank stands out as universally crypto friendly across the region, since relationships shift quickly by country and product line. Some banks participate in limited pilots or serve crypto companies under strict conditions, while others avoid direct exposure altogether. Always check current bank policies and local regulations before opening accounts.

- How do crypto millionaires cash out?

- Large holders typically cash out through regulated exchanges, OTC desks, private brokers or structured sales designed to limit slippage and compliance problems. Identity verification, source-of-funds documentation, banking transfer limits and careful tax planning are all essential parts of the process at significant portfolio sizes.

- Do I need to report crypto gains under $3,000?

- There is no single Latin America-wide reporting threshold. Your obligations depend on your country of tax residence, the transaction type, local tax law and whether the gain qualifies as income or a capital gain. Keep thorough transaction records and consult a local tax professional to understand your specific requirements.

- Do you have to pay taxes on crypto in Mexico?

- Crypto profits can be taxable in Mexico depending on the transaction and your taxpayer status. If you sell crypto for more than you paid, that gain may create a tax obligation under Mexican law. Rules can be nuanced, so consult a qualified Mexican tax professional rather than relying on general guidance.

- Can you invest in crypto in Mexico?

- Individuals can generally access crypto through exchanges and platforms operating in Mexico, though crypto is not legal tender and regulated financial institutions face meaningful restrictions. New investors should account for price volatility, custody risks, potential scams and the importance of maintaining clear transaction records for future tax reporting purposes.

Sources

Author

Crypto analyst and blockchain educator with over 8 years of experience in the digital asset space. Former fintech consultant at a major Wall Street firm turned full-time crypto journalist. Specializes in DeFi, tokenomics, and blockchain technology. His writing breaks down complex cryptocurrency concepts into actionable insights for both beginners and seasoned investors.